4 Home Loan Deal Breakers You Should Pay Attention To

Table of Contents

Found your dream home and now is stressing about committing to a mortgage for most of your life? It can be daunting.

By making the wrong decision on your home loan, can mean lots of trouble and money wasted over the year. Hence, it is important that every home buyer gives this a great amount of consideration. Though that’s a lot easier said than done.

If you do not know what to look out for when reviewing a home loan, you can easily make the wrong decision that can cost you thousands of Ringgit.

With the advent of the Internet, comparing and picking a home loan package is much easier. However, not everyone is aware of the technicalities involved in choosing a loan for their home.

To make it easier, here are some things that you should scrutinise when you are shopping for a home loan in Malaysia:

1. Fixed or variable home loan?

This is a no brainer. It is important but it shouldn’t be the only thing we look at when it comes to mortgage. A low interest rate definitely makes a loan attractive, but it does not automatically make it the best in the market.

Home loan interest rates are dependent on the loan amount and the type of loan (fixed or variable rate). Usually, the higher the loan amount, the lower the interest will be for most banks.

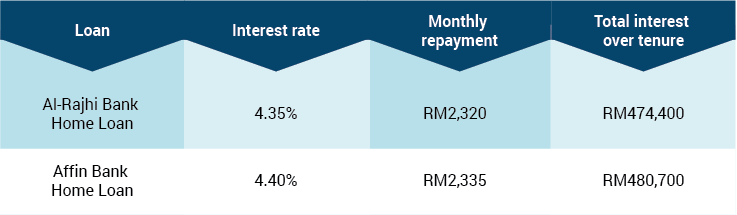

Currently, banks that offer the lowest interest rates are Al-Rajhi Bank, Hong Leong Bank and Hong Leong Islamic Bank at 4.35%, while the highest are are CIMB Bank and CIMB Islamic Bank at 4.95%.

Loan amount: RM500,000

Loan tenure: 35 years

A 0.05% difference in interest rate can result in RM6,300 additional interest based on the example above.

With the recent Overnight Policy Rate (OPR) hike, variable rate loans are looking less attractive compared to the fixed rate home loan provided by AIA. Variable rate loans are tied to the Base Lending Rate (BLR), which in turn is tied to the OPR which can go up or down. When it goes up to higher than what is offered by a fixed rate loan, then it will make it unattractive. However, what goes up have the possibility of coming down again.

A three-year comparison between a variable and fixed home loan showed that if you bought a property in 2012, you would have paid about RM61,545.38 in interest if you take up a variable rate home loan, and RM64,640.75 if you take a fixed rate loan at 4.39%. That’s a RM3,095.37 difference in just three years! However, if OPR is expected to increase again (and again), a fixed rate can be a good option. That’s a risk you’ll have to take.

Remember, a home loan is a long term loan (maximum of 35 years) and you shouldn’t only compare fixed and variable rates at the point of application. It pays to think long term.

Find out more about the interest rates offered by different banks.

2. Flexi or fixed term loan?

There are various types of loans that you can get to finance your property. We wouldn’t say one is outright better than another, each type has its use.

For example, a full flexi loan is good if you do not have a fixed income, where one month can be more than another, or if you are able to deposit more money than you need to into the loan account during the course of your loan period. Any additional payment that you put in will automatically go to reducing the principal account, resulting in lower interest for the rest of the loan tenure.

This home loan is linked to a current account for that reason. However, the current account will incur an additional maintenance fee (usually RM10) every month. That’s RM4,200 to the bank over 35 years — for no reason if you don’t make use of the flexibility.

Similarly a semi-flexi loan allows one to reduce its principal amount by making additional repayments. However, you will need to make a formal request and incur additional charges if you want to withdraw the additional money later on.

If you have a strict and predictable cash-flow pattern, a traditional term loan may be best. For the average Malaysians, it is best to get the semi-flexi loan if you plan to pay more occasionally. However, if you have a stable and and fixed income, there’s nothing wrong with getting a basic term loan, especially if you can get it with better interest rate compared to others.

3. Margin of finance

It’s been three years since the implementation of the new home loan rules where buyers will have to fork out more cash to purchase their third and subsequent property. For buyers who are looking to buy their first or second property, they will stand the chance of getting 90% margin of finance on their mortgage from banks.

However, banks also take various other factors into consideration when putting together their loan offer, such as the value of the property and your credit rating. Different banks may offer you different margins of financing.

The minimum you have to come up with in cash is 10% of the property price. However, if you are unable to secure a 90% margin, then you will have to cough up more cash for down payment.

For example, a RM500,000 property will require RM50,000 (10%) in cash for 90% margin of finance and RM100,000 (20%) for 80%. That’s a big difference.

4. To lock or not?

Are you buying the property for your own occupation or is it for investment? This question will also affect how you choose your home loan package.

If you are buying a property for investment — where you will either lease it or sell it when the value appreciates, a loan with short or no lock-in period will be your best bet.

A lock-in period refers to the period of your home loan where you will be penalised for early settlement. Selling your property or paying off the loan in full within this period will result in penalty of 2% to 3% of the principle loan amount.

A RM500,000 loan can cost RM10,000 in penalty if you sell it during the lock-in period. However, if the appreciation on your property is high then this won’t hurt as much but if not, it is best to wait until the period is over before selling it.

The good thing is, most of the Islamic home loans do not have lock-in periods and the interest rates do not differ in most cases. So, be sure of why you are buying the property and choose the right loan to complement it.

Buying a property should never be taken lightly especially if you are not buying it to sell anytime soon. Most people would have to deal with a property loan for 30 to 35 years, that’s most of one’s adult life. If you get it right the first time, there will be no need to consider refinancing. Choosing the right loan from the right bank is crucial as refinancing can incur additional cost, hence, it is not something one should take lightly.