What Are The Repercussions If OPR Rises Again?

Table of Contents

The recent rise in Overnight Policy Rate (OPR) by 25 basis points (bps) has resulted in the hike in the Base Lending Rate (BLR) by the same percentage. Many property investors and loan borrowers are worried that there will be more increase in the near future. Even though no increment was announced in the Monetary Policy Committee recently, many are still expecting an increase as early as next year.

Will it go up again?

A recent article published by The Star polled 12 economists from different research houses on their views on the OPR movement in the next few quarters. Five out of 12 opined that the OPR would increase again by September 18, 2014 when the Monetary Policy Committee would convene. Even the top research houses are divided in their forecast.

However, the hike prediction did not come true. Even though OPR has risen thrice in March, May and July 2010, at 25 bps each increment, this time the OPR stayed put.

Historically, Bank Negara Malaysia (BNM) would not increase the interest rate by a huge margin as it would hurt the market, hence, the OPR has always been adjusted gradually.

With the reduction of subsidy for petrol and sugar, the increased in electrical tariff and many other hikes, inflation has rose to over 3% today. If the inflation continues to increase, then the OPR will have to be adjusted upwards further.

Based on the market condition today, the OPR may increase again in the next year, by 25 to 30 basis point, which in turn will increase the BLR by the same margin. Experts opined that the BLR will most probably be adjusted a few times next year. Furthermore, with GST set to be implemented in April 2015, we may see another round of interest adjustment.

How will further adjustments affect loan borrowers?

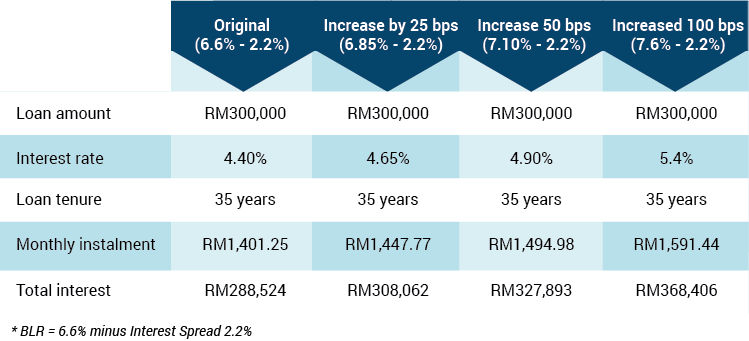

Many loan borrowers are worried of further increase to the BLR. However, 0.25 increase should not significantly affect the loan installment. If the BLR rise more than 100 basis points, then a much greater impact will be seen on loan repayments.

The above calculation shows that the impact of 25 bps on your loan installment for a RM300,000 loan is only an increase of RM46.52. To be realistic, that increment can easily be covered by sacrificing three cups of Starbucks.

The impact is not that great and most people should be able to absorb the difference. Even if the BLR goes up by 50 bps, the loan installment will increase by less than RM100.

And if the BLR were to go up at 100 bps or 1%, than the difference will be larger at RM190 and the total interest payable will see a significant increase of RM80,000 .

What will happen to your loan repayment when BLR rise?

1. Your loan tenure will lengthen but your loan installment will remain the same.

Most home loan borrowers are still paying the same loan instalment amount, even after the hike in the BLR by 0.25%. It’s not a fluke by the bank!

The banks will generally lengthen your loan tenure to the maximum when the BLR is adjusted upwards. Most banks will not send a letter to home owners to give them the options of lengthening the tenure or increasing the loan installment. If you would like to opt for higher instalment instead of longer tenure, you will need to go to the bank and sign the instruction form.

The repercussion of lengthening your tenure is your principal reduction on their original loan becomes minimal. Longer tenure to maintain your original loan installment means you will be paying more towards the interest and lesser to the principal.

This option should be chosen only if you are unable to pay for the increase.

2. Your loan instalment will increase but your loan tenure will remain the same.

This option will be able to save more on the interest payment, compared to the first (and mostly default) option. However, if the increment in instalment is too big and the loan tenure has already been stretched to the maximum, the bank system will automatically increase your loan instalment.

To safeguard your finances from further increase in the BLR, it would make sense to manage your expenses prudently. Cut down on unnecessary purchases and start saving money or increase the percentage of your monthly savings.

With proper management of funds, any increases in the BLR will not have a significant impact on loan borrowers. If these measures are not taken, there will surely be a spike in non-performing loans soon.

Miichael Yeoh with over 18 years of experience in banking and finance, has handled more than 1,000 mortgage cases in his career. Currently, Yeoh is the Director and Founder of GM Training Academy PLT and Victorious PLT. With his vast experience, Yeoh is now a sought-after speaker in property exhibition and developer property launches in Malaysia and overseas. He is also the author of Think Like a Banker, Act Like A Player.