The Impact Of OPR Hike On Your Home Loan

Table of Contents

Though the recent overnight policy rate (OPR) hike has been lauded by analysts and foreign investors as a good move for the Malaysian economy, it has also ignited uncertainties among consumers, especially loan borrowers.

Having to contend with the rising cost of living due to various price hikes and subsidy rationalisations, Bank Negara Malaysia (BNM) now thrust another hike in the form of interest rates to the already staggering level of household debt.

For the uninitiated, the thought of higher monthly repayments on their already struggling mortgage may cause a panic. However, will this really create a huge impact on their wallet in reality?

And will this lead to droves of borrowers defaulting on their loans due to the increase in repayments? iMoney digs further and reveals the potential consequences a mere 0.25% may cause to consumers.

Swift reaction from banks

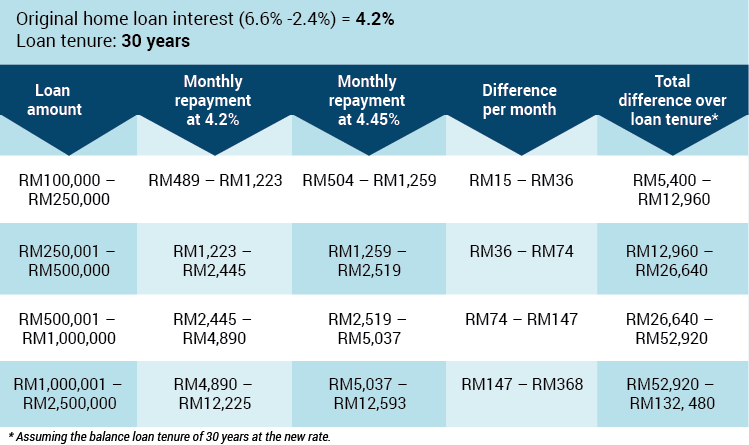

With Maybank and Public Bank leading the way, other major banks are following suit by raising their base lending rates (BLR) and base financing rates (BFR) from 6.6% per annum to 6.85%.

Other than these two banks, others who have confirmed their new rates, which will be effective on July 17, 2014 are Hong Leong Bank Bhd (HLBB), CIMB Group Holdings Bhd, Alliance Financial Group Bhd and OCBC Malaysia.

Banks that have not made any announcement yet are still considering the quantum of the deposit rates, which will impact their earnings eventually.

In a StarBiz report, Akhsan Zaini, senior vice-president and head of distribution of Bank Simpanan Nasional said, “We are still studying the impact of the rate hike on our bank before we announce the adjustment next week, tentatively.”

He also said the bank had yet to decide on how much it would adjust for its deposit rates.

What it means to monthly repayments?

Using iMoney’s latest BLR calculator below, here is how much you will need to pay for your home loan repayment with the latest base lending rate.

JP Morgan Research cautions banks that the combination of rate hikes and subsidy rationalisation would test the credit risk management of Malaysia’s consumer-led loan growth in the past five years.

Another brick in the wall for speculators

In a New Straits Times report, OCBC Bank (Malaysia) Bhd’s head of secured lending Thoo Mee Ling explained that the hike would impact existing and new home loan borrowers whose rates are tied to the BLR.

The increments when divided into monthly repayments doesn’t look too significant, most experts opine that the new OPR will affect property speculators the most.

Unlike genuine home buyers and property investors, most speculators do not have the extra cash to weather any increment in repayments or new regulations.

James Wong, director of VPC Realtors (KL) Sdn Bhd told The Star, “If they [property speculators] are unable to service the loan, they will be forced to sell. But it will not be as easy as before due to the real property gains tax,” he said.

They may not be able to funnel the hike down to their tenants (if they rented out their properties) as rental rates are primarily determined by demand and supply, and will not be affected by interest rates.

Will the property market cool off even further?

With the anticipated goods and services tax (GST), the hike in the overnight policy rate (OPR) will no doubt impact the housing affordability and sales even further.

According to Maybank IB Research in May, it is reported that most developers are already doing GST-related re-pricing and re-costing exercises ahead of the April 2015 timeline and the anticipated higher interest rates, the housing affordability index could decline further.

The report predicted that the OPR hike would lead to a further decline in property sales.

Property consultants also expect fewer transactions in the next few months.

Households and businesses may be more cautious on getting additional loans, according to Affin Investment Bank, referring to the higher inflation and expectations for BNM’s hiking cycle to continue.

Most property buyers and investors will most probably adopt a wait-and-see attitude amidst the uncertainties ahead.