Wedding Loans: The Worst Decision You Could Make

Table of Contents

Everyone has their idea of a dream wedding, but they all have one thing in common. Dream weddings don’t come for free. Unless you have been saving and planning in advance before you (or he) popped the question, chances are you may not be able to afford your dream wedding.

With the rising cost of living, wedding costs see a hike too. In 2014, an average price in a Chinese banquet restaurant will cost about RM988++ per table of 10 pax. However, if you are planning your wedding for 2016, the same menu at the same restaurant, would have spiked to RM1,168 per table. That’s almost 20% up!

If your dream wedding takes place in a five-star hotel in the Klang Valley, the price would be significantly different. For instance, wedding packages at the popular five-star Mandarin Oriental Hotel in Kuala Lumpur would cost you close to RM2,200 per table at the very least, and comes with a minimum requirement of 25 tables – this means you would have to fork out at least RM55,000.

Costlier packages at the hotel would cost you well over RM3,000 per table and come with a minimum requirement of 30 tables. A couple who purchase this package will need to prepare to pay RM90,000 to RM95,000 for a reception at the venue (not including other costs involved).

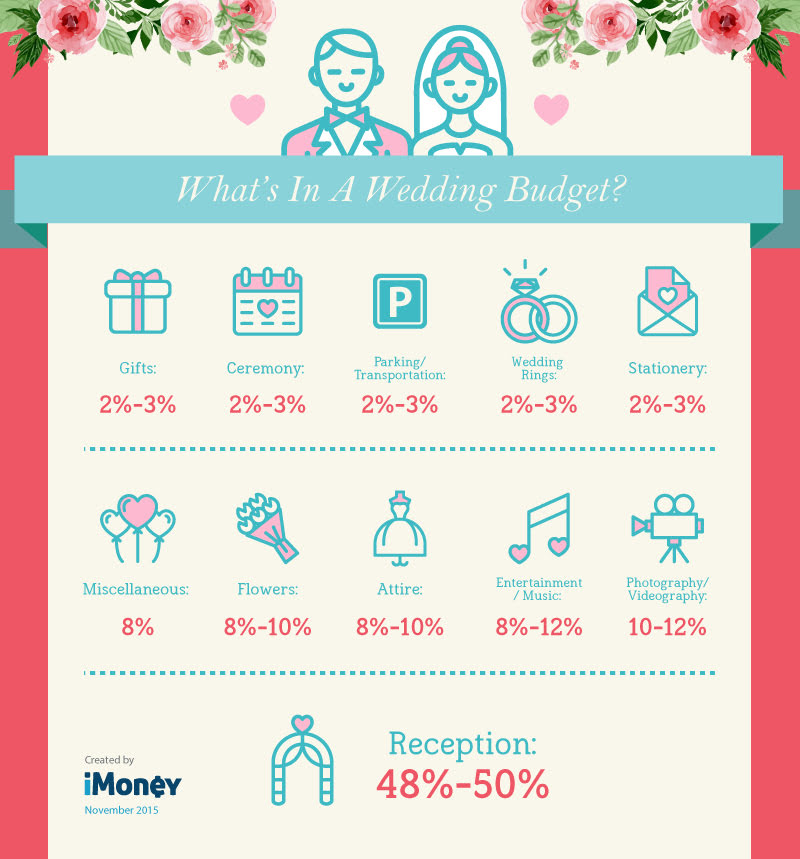

Bear in mind that the reception makes up only half of the wedding average wedding budget!

What do people spend on in a wedding?

According to various wedding websites and available resources, here is a basic budget breakdown of the average wedding in Malaysia:

Seasoned wedding planners estimate that an average wedding in Malaysia would set couples back by at least RM50,000. However, given today’s weaker currency and lifestyle inflation resulting from the Goods and Services Tax (GST), the cost of getting hitched today could have escalated well beyond that.

And this does not include the cost of your honeymoon!

Not surprisingly, soaring wedding expenses have caused some couples to take out personal loans to pay for their nuptials if they are unable to get the financial support they require from their parents.

You may not realise this when you’re caught up in the frenzy of floral arrangements and the sparkly sequins of your designer dress, but taking on debt to pull off your dream wedding may just be the worst idea ever, and here’s why:

Till debt do us part

Money has been cited as one of the top reasons why marriages disintegrate. Unfortunately, money problems could start cropping up way before you even walk down the aisle, if you are not careful.

As is, many young couples enter a marriage carrying their own debt loads. A recent study by the Asian Institute of Finance (AIF) revealed that Malaysia’s Gen Y are experiencing significant financial stress early in life with many living beyond their means and are trapped in emotional spending.

Unfortunately, for many young couples, the debt only increases within the first few years of marriage (and with only 28% of respondents reported of feeling confident in their financial literacy, we’re not that surprised).

What many fail to realise is that splurging on a wedding also often means having to make sacrifices during the beginning stages of your marriages.

In the short term, being bogged down by debt could mean having a relatively uneventful or even troubled newlywed year. And this could mean anything from not being able to travel to your desired honeymoon destination, having to scrooge on wining and dining, or worse, having trouble paying your bills.

Who wants to spend their first year in marriage penny-pinching and stressing over the looming balance of unpaid loans or on your credit cards?

Long term consequences can be more serious. Over time, a huge wad of wedding debt can seriously derail your long-term financial plans and goals.

For instance, if you took out a personal loan for your wedding, having outstanding debt can affect your credit score and make you a less desirable candidate when it comes to applying for a mortgage or a car loan.

You could be denied a loan completely or get stuck with a less favourable interest rate, which will affect your finances for many years down the road.

It gets trickier when you want to start a family, as having children will no doubt add a whole new dimension of debt and financial burden.

So if you look at the grand scheme of things, not only can wedding debt spoil your plans, it can also add layers of stress on your marriage down the line. Hence, before you sign up for a personal loan, ask yourself whether a single day – as magical as you want it to be – is worth many years of financial tension and sacrifice.

Avoid the wedding debt trap

Plan ahead

We don’t mean to be Captain Obvious, but planning a big event like this in advance will not just save you a lot of headaches, but also money, especially since banks typically charge 12% to 15% per annum (p.a.) for personal loans.

This means that if you take out a RM10,000 loan, at a rate of 15% p.a., you would have to pay a staggering RM1,500 more in just the first year. This rolls into larger amounts the longer the repayment period is as well!

How to avoid doing this? Start saving for your big day early, and this could be before you even meet that special someone. It can seem inconvenient or even stressful at first (and then there is the all-important matter of meeting the right person), but last minute planning and execution is the mother of all financial stresses, and you don’t want that for your wedding, do you?

You can’t control the universe, but you can make that financial planning bit just that much easier by setting aside a fixed amount every month for what would be one of the most memorable events in your lifetime.

You may think that you don’t plan on getting married anytime soon but you need to be ready when that day comes because you can’t stop love. Besides, having more time to save is actually a good thing.

(If all fails, you can always spend your hard-earned money on your cats.)

Stalk wedding expos

Look out for wedding exhibitions or expos where you will be able to scout for good deals and packages that could help you save considerably.

There will also be a variety of booth and companies for you to choose from, and you will probably be able to compare prices, learn more about the industry and ultimately, secure the best deals.

You will likely be able to get promotions at a discounted price or a special rate, but make sure you read the fine print and clarify details you require before you sign any agreement or make any upfront payments.

Sites like Wedding.com.my also allows couples to browse through wedding vendors and merchants in Malaysia’s wedding industry and secure the best deals online.

Learn to DIY

Want a fancy wedding but your budget doesn’t quite allow for it? You can still find a way to work around it by learning how to do things yourself.

For instance, you will probably be able to save a few hundred bucks on printing costs alone if you choose to go with electronic wedding invitations. You will be able to find available templates online and even on Pinterest.

You can also do your own decorations or hand-make items such as your bridal bouquet for a personal touch.

Don’t know where to start? Local sites like The Wedding Notebook and Bridal Guide should give you plenty of ideas and inspiration for your wedding day.

Get as much done on your own as possible to reduce those fees.

Leverage on your wedding expenses

This is a tricky one but If you are able to service your credit card payments in full each month, consider getting a new credit card just for the wedding.

Look out for one that will reward you for your spending such as reward points or cashback incentives, or one that will earn you airline miles. It’s not just a good way to accurately keep track of your wedding expenses, it can also help pay for some of your honeymoon expenditures.

For instance, the OCBC Platinum MasterCard lets you earn 0.5% cashback on all retail transactions without a cash back limit. Meanwhile, the HSBC Amanah Advance Visa Platinum offers up to 1% in cashback on retail spending.

Elsewhere, the Standard Chartered WorldMiles Card lets you earn airline miles that can be converted into MAS, Singapore Airlines or AirAsia miles.

If you play your (credit) cards right, you will be able to take advantage of the perks and actually get some money back while you spend! Just remember that you need to be able to pay these off in full in order to maximise the benefit. Otherwise you’ll be worse off than taking a personal loan!

Many couples feel that the wedding costs are justified because it is (in theory) an once-in-a-lifetime occasion. While it is easy to get caught in a nuptial frenzy, it is important that you do not overspend on your wedding so you can stroll happily down the aisle together and have a debt-free ever after.

At the end of the day, what is most important is security, and financial safety often ranks at the top of the list, which is why working together on how to have an enjoyable yet affordable wedding is a great lesson in how you will manage your money well into marriage.