Should You Be Debt-Free Or Free Of Bad Debt?

Table of Contents

For even the most frugal and financially-able person, taking on debt is inevitable.

In fact, Malaysia’s household debt is one of the highest in the region, reaching 89% in 2021. According to Bank Negara, this translates to nearly RM1.4 trillion worth of debt burden being carried by Malaysians.

But is being debt-free really the ultimate goal or should Malaysian focus on being bad-debt-free?

At its most basic definition, debt is simply an amount of money borrowed by one party from another. This definition in no way indicates that debt is good or bad. However, a closer look shows two types of indebtedness – good debt and bad debt.

A good debt basically means using money to make more money. For example, a home loan can be considered a good debt as it appreciates over time, resulting in profit or return in the future.

However, bad debt, in general, refers to debt that won’t go up in value or generate income. Most people consider a car loan a bad debt as car value typically depreciates over time.

In some cases, even a good debt can turn in a bad one – when it is left unmanaged. No doubt, unmanaged debt can ultimately lead to bankruptcy, but there are ways to circumvent that end.

Here are five things you should avoid to prevent your debts from spiraling out of control:

1. Paying only the minimum payment on your credit card

According to Bank Negara data, Malaysians outstanding credit card balances rose to RM35.89 billion in July 2022. An earlier survey had also highlighted that only 15% of Malaysian credit cardholders pay above the minimum required amount of 5% of total outstanding balance every month.

Paying more than the required minimum is paramount to being debt-free as quickly as you can. In fact, paying off your credit card debt in full can take decades if you only pay the required minimum amount every month (assuming you are not charging additional debt on top of the existing one)!.

2. Paying high credit card interest

Assuming you currently have an amount outstanding on a credit card that charges you an annual interest of 15% and have a habit of making prompt payments; consider taking up a Balance Transfer facility.

Transferring your current outstanding balance to a credit card that charges a lower interest rate can expedite your loan settlement.

3. Taking up loans with long tenures unnecessarily

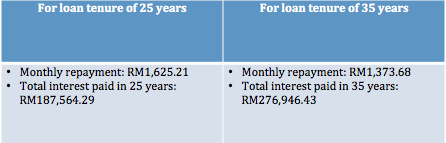

You are allowed a maximum loan tenure of 10 years for a personal loan and 35 years (not exceeding the age of 65 at the end of the loan tenure) for a home loan in Malaysia.

Longer loan tenures allow you the privilege of lower monthly repayments but at the cost of a larger total repayment at the end of the loan tenure. So, while you save a little every month, you end up paying more in the end.

For example, you might have a RM300,000 home loan at an annual interest rate of 4.25%:

Saving RM251.53 a month (RM30,183.60 over 10 years) will cost you an excess of RM89,382.14 in total interest paid.

4. Managing too many debts

Debt management plays a huge role in your endeavour to be debt-free but keeping track of what you owe can be difficult if you have multiple debts (e.g. personal loan, credit cards, and overdrafts).

To better manage all your debts, consider debt consolidation. Debt consolidation is the act of moving all outstanding debt balances to one place. This makes it easier to manage your debts, thus avoiding penalties from late or missed payments.

5. Leaving debt management to the last minute

While the tips above can help most achieve debt-free status, for some it is a little too late to be practising them.

However, there is still hope even if your debt problems are getting the better of you.

Credit Counselling and Debt Management Agency (AKPK) is an agency set up by Bank Negara Malaysia to educate individuals on responsible use of money and credit management skills, provide counseling and advice on financial management, and assist consumers in regaining financial control through a debt management programme. These services are provided for free.

Being debt-free may be overrated and slightly unrealistic in this day and age. Not all debts should be avoided. The point in case is to always consider all your options before taking up a loan and ensure you can commit to it throughout the loan tenure.

Knowledge, discipline, and a change in lifestyle are no doubt essential components in your journey to being bad-debt-free but stick to it and the result will be financial freedom and restful nights.

Need help with debt management? Find out more details from AKPK.