How Does Base Lending Rate (BLR) Affect Your Home Loan?

Table of Contents

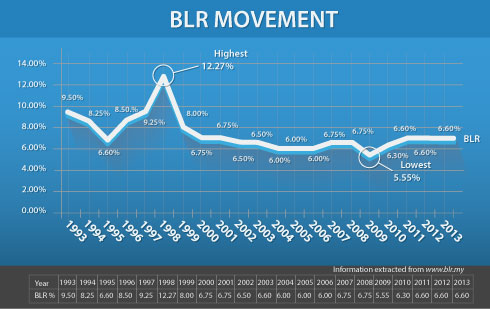

Malaysia recorded its highest ever Base Lending Rate (BLR) of 12.27% in 1998 before rising and falling to its lowest recorded BLR of 5.55% in 2009. Below is a graph showing the movement of Malaysia’s BLR in the last 20 years (1993 – 2013):

What is it?

If you’re a seasoned home buyer, BLR is something that needs little to no introduction. But if you’re applying for a home loan for the very first time, you’re probably wondering what it is and why it’s such a major concern.

In layman’s terms, BLR is the base interest rate that banks refer to internally before deciding how much to charge (i.e. interest rate) for your home loan.

However, a more accurate definition of the term is that it is a rate determined by each bank based on how much it costs to borrow the money to be lent to borrowers. The cost to borrow money is determined by the Overnight Policy Rate (OPR) – the interest rate at which other banks lend to each other.

Recap: Base Lending Rate (BLR)

- Determined by Bank Negara Malaysia (BNM)

- Based on internal cost of funds (i.e. how much it costs to borrow the money to be lent out)

- Changes to the rate are affected by changes in the OPR

The OPR is determined by BNM which decides whether to move this rate up or down depending on the current state of global economy and its objectives. Generally, it rises when the money market is on an uptrend and falls when the opposite happens.

What does the % mean?

Knowing what the prevailing BLR is will help you make sense of interest quotations by banks. When seeking for a home loan, banks will often quote an interest rate of BLR plus or minus a percentage.

Below is an example of how to make sense of interest quotation by banks:

What’s in store in the future?

With the recent hike in the OPR by 25 basis points, most experts are not expecting further hike in 2014.

Malaysian Institute of Economic Research (MIER), a local economic think tank, said it is not expecting any further hikes in the OPR for the rest of the year.

“Real interest rate is in the negative still but there may not be another hike. Not in the immediate future. Twenty-five basis points is enough for now,” said MIER ED Dr Zakariah Abdul Rashid in a report on The Malaysian Reserve.

Bank Negara Malaysia has also announced a new interest rate framework known as the Base Rate that is set to replace the current BLR rate in 2015.

How does the recent hike affect you?

Any changes would impact floating rate loans which are common for mortgages. While the effect of the new Base Rate framework is still unclear, the increase in OPR has definitely affect the rates charged by banks for home loans for the simple reason that banks adjust their lending rates by a similar quantum when OPR changes.

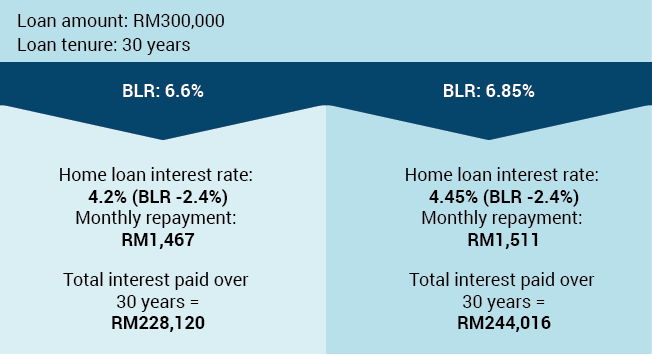

Here is how the increase in the lending rate (as a result of an increase in OPR) has affected your total interest paid if you currently have a floating rate home loan.

Based on the calculations above, a mere 0.25% increase in lending rate has resulted in a 7% increase in total interest paid over the loan tenure.

What can you, as a borrower, do?

As a borrower, you can always negotiate for better rates, especially when you have a strong case to do so. However, this is subject to the following criteria:

- having a good track record with the bank

- being a priority banking customer

- having documentations proving you have high net worth

- buying high-value properties

Ultimately, to better protect yourself from fluctuations in BLR, taking-up or refinancing to a fixed term home loan is a wiser move. iMoney’s home loan calculator and comparison tool can help you find the best fixed rate home loan.

UPDATE: The article was updated to reflect the recent OPR hike by 25 bps.