Best Personal Loans In Malaysia: Guide To The Top Options Based On Your Need

Table of Contents

Good news, we are here to help you discover the best personal loans in Malaysia, tailored to your needs. From business expansion to housing renovations, we have prepared a comprehensive guide to help you find the perfect fit for your financial journey.

If you pick a loan that matches your needs and repayment ability, it could help you reach your goals faster. However, finding the right loan that suits you can be a daunting task.

So, we have put together a list of loans to match the top purposes for a personal loan. In order to help you decide, we have also grouped personal loans based on their top features to suit your needs.

Here are the top options based on the purpose of your loan:

| Best option for: | Product | Loan/ Financing amount | Interest/ Profit rate | Loan/ Financing tenure | Min. monthly salary | Apply online |

|---|---|---|---|---|---|---|

| Debt consolidation | Alliance Bank CashFirst Personal Loan | RM5,000 – RM300,000 | 4.99% - 8.38% | 1 – 7 years | RM3,000 | Apply Now |

| Financial emergencies | RHB Personal Financing | RM2,000 - RM150,000 | 7.19% - 13.83% | 1 – 7 years | RM1,500 | Apply Now |

| Housing renovation | Al Rajhi Bank Personal Financing-i | RM10,000 - RM250,000 | 5.37% - 11.51% | 1 – 8 years | RM5,000 | Apply Now |

| Business expansion | Alliance Bank CashFirst Personal Loan | RM5,000 – RM300,000 | 4.99% - 8.38% | 1 – 7 years | RM3,000 | Apply Now |

We have also complied a list of personal loans based on their product features for comparison for your convenience.

Here are the top options based on the features of the loan:

| Best option for: | Product | Loan/ Financing amount | Interest/ Profit rate (p.a.) | Loan/ Financing tenure | Min. monthly salary | Apply online |

|---|---|---|---|---|---|---|

| Fast approval | RHB Personal Financing | RM2,000 – RM150,000 | 7.19% - 13.83% | 1 – 7 years | RM1,500 | Apply Now |

| Lowest interest/ profit rate | Bank Islam Personal Financing-i | RM10,000 - RM300,000 | 4.5% – 6.99% | 1 – 10 years | RM4,000 | Apply Now |

| Lowest income requirement | Agrobank AgroCash-i | RM10,000 – RM250,000 | 3.45% – 3.95% | 2 – 10 years | RM1,000 | Apply Now |

| Longest loan tenure | Bank Rakyat Personal Financing-i Private Sector | RM5,000 - RM400,000 | 5.37% - 5.47% | 5 – 10 years | RM2,000 | Apply Now |

| Highest loan amount | Alliance Bank CashFirst Personal Loan | RM5,000 – RM300,000 | 4.99% - 8.38% | 1 – 7 years | RM3,000 | Apply Now |

| Govt. employees | BSN MyRinggit (Public Sector) | RM5,000 – RM400,000 | 2.53% - 8.85% | 1 – 10 years | RM1,500 | Apply Now |

| Islamic financing | Alliance Islamic Bank CashVantage Personal Financing-i | RM5,000 – RM300,000 | 4.99% - 8.38% | 1 – 7 years | RM3,000 | Apply Now |

Sticking to your financial resolutions in the past year may have been more challenging than before but it doesn’t mean you have to give up on that much-needed home renovation or great business idea you have in mind.

Want to know which are the best personal loans available in 2024? We have curated a list of personal loans best suited to meet your needs and requirements.

1. Best personal loan for business expansion

According to the Global Startup Ecosystem Report 2023, Malaysia is among the countries recognised as having an emerging startup ecosystem. More and more Malaysians are diving into the world of entrepreneurship and developing their own business.

In the case that you can’t secure a grant or an investor, a personal loan like the Alliance Bank CashFirst Personal Loan can be the next best solution.

| Alliance Bank CashFirst Personal Loan | |

|---|---|

| Interest rate | 4.99% - 8.38%% |

| Loan amount | RM5,000 – RM150,000 |

| Loan tenure | 1 – 7 years |

| Approval duration | Up to 24 hours |

| Minimum income requirement | RM3,000 a month or RM36,000 per annum |

| Age requirement | 21 – 60 |

Strengths: You can borrow up to eight times the amount of your fixed monthly gross income. It’s also one of the few personal loans that allows self-employed individuals to apply.

Drawbacks: If you’re self-employed, you need to have been in the business for more than two years in order to apply. Interest rates could also skyrocket to as high as 14.78%, depending on your credit profile and loan tenure.

Alliance Bank CashFirst Personal Loan

Interest rates as low as 4.99% p.a.

Approval within one working day2. Best personal loan for housing renovations

If you have made a home purchase or have an old home you would like to spruce up, personal financing can help with funding the contractor or other home maintenance work.

Renovating your home can also increase your property’s worth, which is beneficial if you are opting to sell it off within a few years.

Hence, pick a personal financing plan, such as Al Rajhi Bank Personal Financing-i, that won’t strain your budget in the long term by opting for a longer tenure and a low profit rate so that it’s less costly.

Furthermore, the repayment amount will be less if your financing tenure is longer, which is why this plan is the best to furnish your home.

| Al Rajhi Bank Personal Financing-i | |

|---|---|

| Profit rate | 5.37% - 11.51% per annum |

| Financing amount | RM10,000 - RM250,000 |

| Financing tenure | 1 – 8 years |

| Approval duration | 2 days |

| Minimum income requirement | RM5,000 a month, but subject to a minimum annual income of RM60,000 |

| Age requirement | 21 - 60 years old |

Drawbacks: You must earn at least RM60,000 a year to qualify for the plan and be a fixed-income earner. Also, if you have a bad credit reputation, you must settle all overdue payments before applying as there are no exceptions for applicants with a bad credit record.

Al Rajhi Bank Personal Financing-i

Profit rates start from 5.37%

Flexible tenure of 1 to 8 years3. Best personal loan for debt consolidation

If you are among those with multiple obligations, you can ease your burdens by consolidating your debts. Your best bet would be a personal financing plan. For this category, we also chose the Alliance Bank CashFirst Personal Loan.

Strengths: When you’re paying off multiple debts, you’ll want to consolidate them under lower interest rates, so you can reduce your interest payments. The Alliance Bank CashFirst Personal Loan has relatively low interest rates that start from 4.99%. Its minimum income requirement of RM3,000 is also lower than some personal loans.

Drawbacks: Consolidating your debts under this loan may only be worth it if you are eligible for the best interest rates. Otherwise, interest rates can go up to 14.78%.

Alliance Bank CashFirst Personal Loan

Interest rates as low as 4.99% p.a.

Approval within one working day4. Best personal loan for financial emergencies

Sometimes unfortunate events can drain the life out of your bank account, which is why personal loans are your best bet in the event of an emergency, such as an urgent medical procedure.

If you don’t have the facilities to meet the high cost of your emergency, such as not having insurance, a personal loan with a fast approval rate can provide the cash you so badly need without the usual lengthy process. RHB Personal Financing is great for this.

| RHB Personal Financing | |

|---|---|

| Profit rate | 7.19% - 13.83% per annum |

| Financing amount | RM2,000 - RM150,000 |

| Financing tenure | 1 – 7 years |

| Approval duration | 10 Minutes |

| Minimum income requirement | RM1,500 a month |

| Age requirement | 21 - 55 |

Drawbacks: You must open a linked bank account and those with a bad credit record must settle their overdue payments to qualify. The interest rate could also go up to 13.83% per annum and there will also be a 1% late penalty fee on your outstanding amount.

RHB Personal Financing

Fast approval within 10 minutes

Minimum income requirement of RM1,500 a month5. Best personal loan for government servants

As a government servant, you could qualify for personal loans that offer you lower interest rates and waived fees, such as BSN MyRinggit (Public Sector).

To qualify for lower interest rates, you’ll need to be a full-time civil servant who has served at least three months, or you are a contract worker with over 12 months of serving in the government sector / GLA / GLC / organizations which has the facility of salary deduction through BPA.

| BSN MyRinggit (Public Sector) | |

|---|---|

| Profit rate | 2.53% - 8.85% per annum |

| Financing amount | Up to RM400,000 |

| Financing tenure | 1 – 10 years |

| Approval duration | 5 working days |

| Minimum income requirement | RM1,000 a month |

| Age requirement | 18 – 60 |

Drawbacks: Personal loans for government servants strictly require that you are employed in the government sector / GLA / GLC organizations for you to qualify for their specific financing product.

BSN MyRinggit (Public Sector)

Profit rates 2.53% – 8.85% p.a.

Get financing of up to RM400,000!6. Best personal loan with the fastest approval

Sometimes life takes you by surprise, and that surprise could be in the form of a financial emergency. If you are stuck in a similar situation, personal loans with fast approval are available, so you don’t have to worry about coming up with money for sudden emergencies. The best personal loan with the fastest approval duration is: RHB Personal Financing.

| RHB Personal Financing | |

|---|---|

| Profit rate | 7.19% - 13.83% per annum |

| Financing amount | RM2,000 - RM150,000 |

| Financing tenure | 1 – 7 years |

| Approval duration | 10 Minutes |

| Minimum income requirement | RM1,500 a month |

| Age requirement | 21 - 55 |

Drawbacks: A penalty of RM200 is imposed for early settlement within first six months, so you cannot avoid interest even if you settle your debt early. There is a one-time 0.5% stamp duty fee on application. You will need a linked account and hold Malaysian citizenship. The interest rate is on the higher side of the loan market and late payment charges will be 1% of the outstanding amount.

RHB Personal Financing

Fast approval within 10 minutes

Minimum income requirement of RM1,500 a month7. Best personal loan with the lowest interest rate

If time is on your side, look for the personal loan with the lowest interest rates. A lower interest rate means a lower cost of borrowing. For example, a personal loan with a 7.00% interest rate costs only RM6,288 over three years for a RM30,000 loan, while a loan at 12.00% costs RM10,788 over the same period.

We’ve combed the market and found the personal loan with the lowest interest rate: Bank Islam Personal Financing-i (Non-Package).

| Bank Islam Personal Financing-i (Non-Package) | |

|---|---|

| Profit rate | 4.5% - 6.99% per annum |

| Financing amount | RM10,000 - RM300,000 |

| Financing tenure | 1 – 10 years |

| Approval duration | Up to 5 business days |

| Minimum income requirement | RM4,000 a month |

| Age requirement | 18 – 60 |

Drawbacks: Don’t bank on it for quick cash, as it takes up to five days to process your loan application. It also comes with a relatively high salary requirement of RM4,000 a month compared to other loan services offered in the market. Late payment charges are 1% of your outstanding loan amount.

Bank Islam Personal Financing-i (Non-Package)

Profit rate from 4.50% p.a.

Financing up to RM300,0008. Best personal loan with the lowest income requirement

Most banks prefer to offer loans to higher-income earners or those with better credit health. However, some banks cater to individuals with low or moderate income who need personal loans for emergencies or to start small businesses, making Agrobank AgroCash-i as one solid option.

| Agrobank AgroCash-i | |

|---|---|

| Profit rate | 3.45% – 3.95% per annum |

| Financing amount | Up to RM250,000 for Government servants; up to RM100,000 for GLC staff |

| Financing tenure | From 2 to a maximum of 10 years |

| Approval duration | Up to 5 working days |

| Minimum income requirement | RM1,000 for Government servants; RM2,000 for GLC staff |

| Age requirement | 18 – 60 or up to retirement age (whichever is earlier) for Government servants; 21 – 60 or up to retirement age (whichever is earlier) for GLC staff |

Drawbacks: AgroCash-i has a longer approval process of up to 5 days, making it unsuitable for urgent needs. Eligibility is limited to Government or GLC employees. Contract Government staff require a guarantor from permanent Government employees. Additionally, there’s an RM50 fee for each tawarruq transaction, subject to 6% GST.

Agrobank AgroCash-i

Profit rates from 3.45% to 3.95% p.a.

Minimum income requirement of RM1,000 for government servants9. Best personal loan with the longest loan tenure

A longer loan repayment period results in smaller monthly payments. This option suits those borrowing large sums but can only repay small amounts monthly.

Since July 2013, Bank Negara Malaysia has limited personal loan terms to a maximum of 10 years. We recommend the Bank Rakyat Personal Financing-i Private Sector personal loan as the best option under this category.

| Bank Rakyat Personal Financing-i Private Sector | |

|---|---|

| Profit rate | 5.37% - 5.47% per annum |

| Financing amount | RM5,000 up to RM400,000 |

| Financing tenure | 5 – 10 years |

| Approval duration | Up to 3 working days |

| Minimum income requirement | From RM2,000 (package-dependent) |

| Age requirement | 18 – 60 (at financing tenure's end) |

Drawbacks: The long approval duration may inconvenience borrowers who need funds urgently. Additionally, there is a requirement to pay 0.5% of the total financing amount for stamp duty, which could be a consideration for potential applicants.

Bank Rakyat Personal Financing-I Private Sector

High financing amount with low income requirement

Profit rate from 5.37% to 5.47% p.a.10. Best personal loan with the highest loan amount

Alliance Bank CashFirst Personal Loan offers high borrowing capacity, competitive rates, and flexible terms. It stands out with its generous loan amount, quick approval process, and excellent customer service.

This loan is ideal for those needing substantial funds for large expenses or debt consolidation, making it a top choice for significant personal financing needs.

| Alliance Bank CashFirst Personal Loan | |

|---|---|

| Interest rate | 4.99% - 8.38%% |

| Loan amount | RM5,000 – RM150,000 |

| Loan tenure | 1 – 7 years |

| Approval duration | Up to 24 hours |

| Minimum income requirement | RM3,000 a month or RM36,000 per annum |

| Age requirement | 21 – 60 |

Drawbacks: Self-employed individuals must have been in business for more than two years to apply. Interest rates may rise to as high as 14.78%, depending on your credit profile and loan term.

Alliance Bank CashFirst Personal Loan

Interest rates as low as 4.99% p.a.

Approval within one working day11. Best Islamic personal financing

Alliance Islamic Bank’s CashVantage Personal Financing-i is the top Shariah-compliant personal financing option in Malaysia. It offers competitive rates, flexible repayment terms, and adheres to Islamic principles.

The bank’s transparency, ethical practices, and efficient application process make it convenient for customers to access funds quickly. This product aligns financial decisions with personal values, making it ideal for those seeking principled personal financing in Malaysia.

| Alliance Islamic Bank CashVantage Personal Financing-i | |

|---|---|

| Profit rate | 4.99% - 8.38% per annum |

| Financing amount | RM5,000 - RM300,,000 |

| Financing tenure | 1 – 7 years |

| Approval duration | Up to24 hours |

| Minimum income requirement | RM3,000 a month or RM36,000 per annum |

| Age requirement | 21 – 60 |

Drawbacks: Self-employed individuals must have been in business for more than two years to apply. Interest rates may rise to as high as 14.78%, depending on your credit profile and loan term.

Alliance Islamic Bank CashVantage Personal Financing-i

No processing fee, guarantor or collateral required

Profit rate from 4.99%This article has been updated on September 6, 2024.

FAQs: Frequently Asked Questions on Personal Loan

Check out the most common queries our readers are asking about personal loans in Malaysia:

Personal loans are versatile, unsecured financial tools that can help you achieve goals or cover unexpected expenses. They involve borrowing a fixed amount from a lender, and repaying it in monthly installments over a set period with fixed or variable interest rates, without requiring collateral. If approved, you’ll receive a lump sum to use as needed. Personal loans offer flexibility and convenience, suitable for various purposes such as debt consolidation, home improvements, or medical expenses. This makes them an ideal solution for many financial situations.

When getting a personal loan, consider multiple factors beyond the interest rate. Evaluate loan terms, fees, and repayment flexibility. This holistic approach will help you choose the option that best suits your financial needs and goals.

Interest rates

As with any loan, the lower the interest rate the better. Although most personal loans offer a fixed rate, some offer effective interest rates. Essentially, for a borrower who intends to pay the loan on schedule for the whole tenure, there isn’t much of a difference in the payments.

However, if you are planning to clear off your loan before the tenure is up, a fixed-rate loan may just save you some cash.

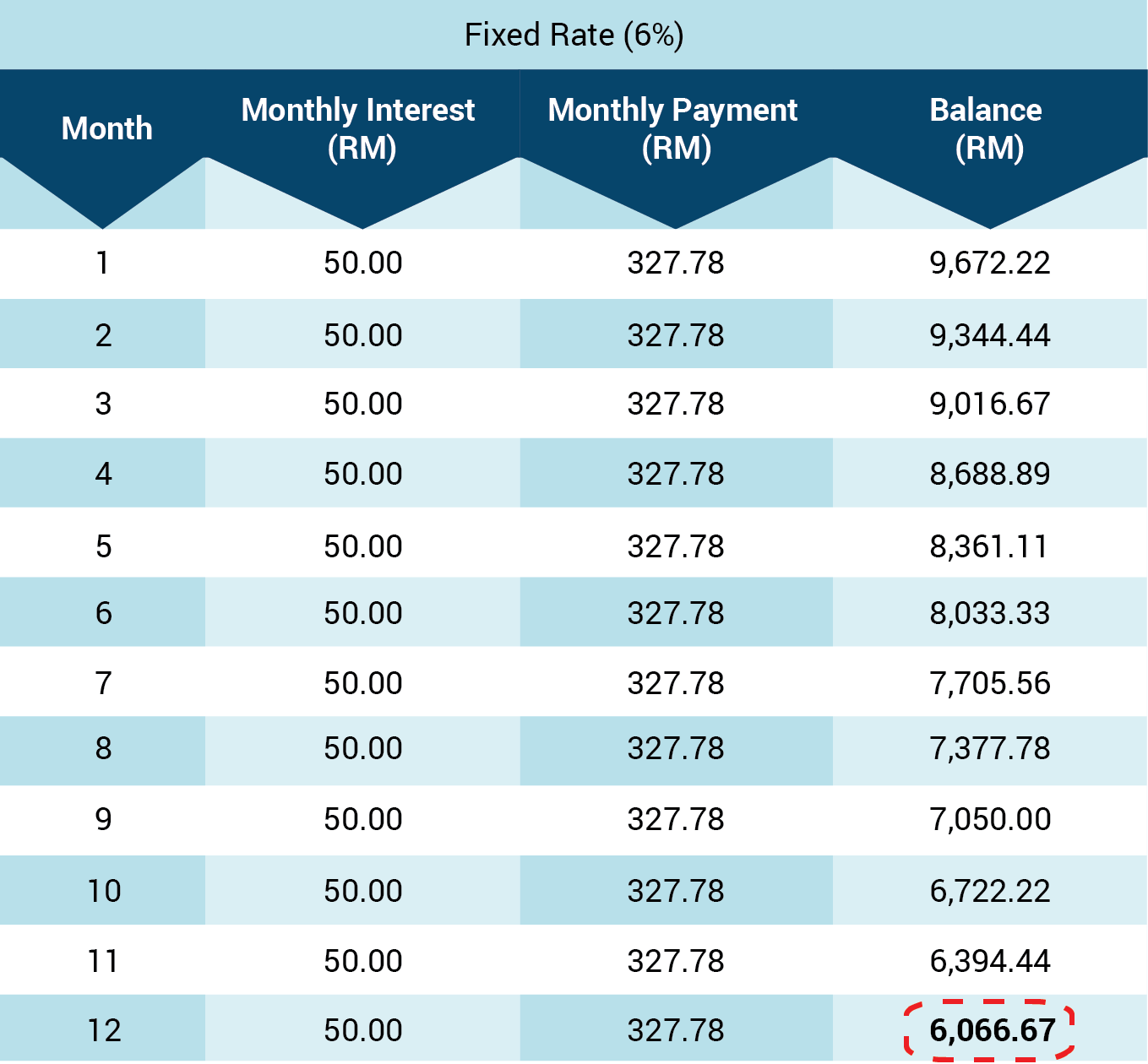

Fixed rate loan

For example, if you are borrowing RM10,000 for a 3-year loan and you would like to pay off your loan in the first year, here’s how much you have to pay for fixed-rate and effective-interest rate loans:

Loan amount: RM10,000

Annual interest rate: 6%

Loan tenure: 3 years

At the end of the first year, you will need to pay RM6,066.67 to clear your loan.

Effective rate loan

At the end of the first year, you will need to pay RM6,864.06 to clear your loan, which is RM797.39 more than the fixed rate.

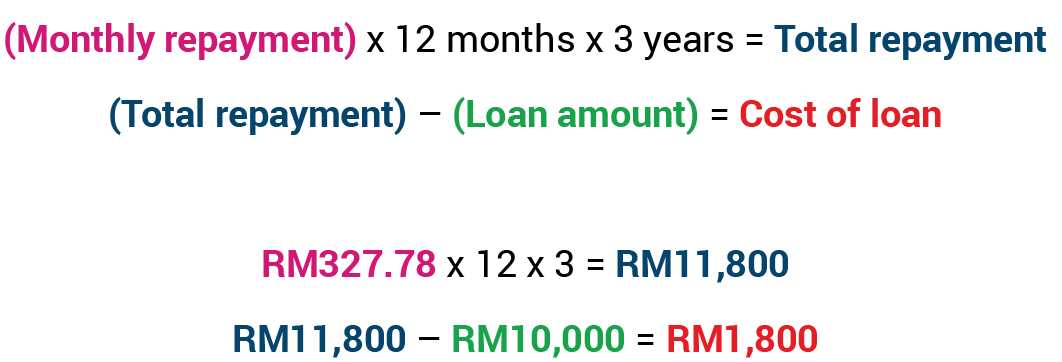

Loan cost

However, we cannot just take up a loan solely based on the interest rates. Sometimes the lowest rates offered may not be the best offer.

To find out if the loan is worth taking out, calculate the cost of your loan. Just check the monthly repayment using our online calculator. In the example above, with 6% rates per annum, you will be paying RM1,800 over three years.

Loan tenure

As of March 2013, Bank Negara Malaysia (BNM) restricted the maximum loan term for personal financing to 10 years. Though it is the maximum tenure allowed, most banks do not allow a 10-year term on their loans.

Some banks do state that the maximum tenure is 10 years. These include BSN, Bank Islam, Maybank (salary financing product), Co-opBank Pertama and Bank Rakyat (Financing-i Public Sector). However, it is not a guarantee that you will qualify for the maximum loan tenure.

Loan amount

Depending on your financial need, you may need to look for a bank that lends enough to cover your situation, so check the maximum loan amount first.

The interest rates vary wildly, depending on the loan amount but avoid anything above 10% if at all possible. The maximum loan amount offered currently is RM150,000 and the minimum is RM1,000.

Whichever amount you decide to apply for, always make sure that you will be able to commit to the monthly repayment.

Other costs

Certain personal financing packages require processing fees, stamp duty (maximum 0.55% of the loan amount) disbursement, and other miscellaneous fees. These are all one-time costs to be paid before disbursement.

Other considerations include the option for early settlement of the loan. Some banks require borrowers to pay RM200 or a sum equivalent to 3% of the outstanding loan amount, whichever is higher for early settlement within the first half of the loan tenure. If your loan tenure is three years and you settle your loan within the first 1.5 years, this penalty will be imposed.

Most banks also charge late payment charges of about 1% of the outstanding loan amount. If your outstanding balance is RM6,000, it will be RM60, which can be quite costly if you often miss your payment due date.

Repayment process/options

Personal loan repayment involves regular payments covering principal and interest. Lenders offer various repayment methods:

- Automatic bank transfers

- Manual online payments

- Check payments

- In-person payments at branches

Repayment details are outlined in the loan agreement. Many lenders allow flexible payment due dates. Consistent, timely repayments avoid extra charges and improve your credit score. Understanding and following the process aids financial freedom and creditworthiness.

You may apply for your personal loan online. If you are considering applying for a personal loan, you can avoid the inconvenience of visiting the bank branch and send in your application online instead.

Additionally, you can also further compare loans with our comparison table and leave your details so that our consultants can assist you with your loan application.

However, before you make the leap, here are three things you should consider before you hand over your documents.

- A good credit report– as we’ve mentioned in some of the drawbacks, some personal loans make no exceptions for those with overdue payments or a bad debt repayment record. It is advisable that you settle any overdue payments and stabilise your credit report before you send in your application.

- Make sure you have the means to sustain a loan– to avoid any extra charges, check your financial health and make sure you can sustain the loan itself. If you are planning to take a personal loan, set out a monthly budget and calculate within your means to ensure you have enough cash at the end of the month to pay the loan. Furthermore, some loans will impose a late payment fee if you do not pay on time.

- Speak to consultants – avoid applying on impulse and consult a professional regarding personal loans if you are still not sure of it. You must understand the decision you are making, which you can easily do by getting free advice from our experts via our personal loan page.

Remember: before taking up a personal loan, do your research to understand what you’re getting yourself into. Make sure it’s something you need, and that you can afford the monthly repayments.

iMoney helps you find the best personal loan for your needs while offering a seamless online application process.

Where we stand out:

- Personal loan calculator: Compare and find suitable loans based on your affordability and eligibility.

- Friendly customer care agents: Ready to help guide you through the entire process from checking your eligibility, recommending appropriate loans, and preparing documentary requirements.

- Quick online applications: Apply easily from home, with most processes fully online. Our customer care agents are ready to assist you throughout, from eligibility checks to application submission.

Banks will require you to be at least 18 years old but below 60 years old, and have a current source of income. Some loans may be restricted for full-time employees of private organisations, while others may be open to government servants and self-employed individuals.

Borrowers may also be required to have a linked savings account at the bank or purchase a Takaful product with the bank before they can apply for a personal financing with the bank.

However, not every loan service requires all that. To choose the ideal loan, the borrower will need to weigh all pros and cons and find one that suits their needs.

Although many companies can lend up to RM100,000 or more, you should be careful and conservative when choosing an amount to borrow. Keep in mind that the best personal financing is intended to help you out in a crisis but because of its high interest rates and short payback terms, it is never an ideal long-term financial solution.

Using our personal loan calculator, compare and consider all the loans and options. It can help you make a smart decision when it comes to choosing a personal loan. If you borrow responsibly and pay the loan back in a timely manner, you won’t go wrong.

These loans are not financially beneficial or cheap; they’re simply good for quick emergency cash.

We have recently launched the iMoney Application Tracker, making it easier for the users to track their submitted applications.

[application tracker snapshot]

![]()

The application tracker is a user-friendly tool on the iMoney website. To use it:

- Log in or sign up on iMoney.

- Click the “Tracker” tab.

- View your applications and their statuses.

The tracker provides real-time updates until your application is complete. For more financial product information, compare and apply on iMoney.

The approval process can take 48 hours to a few days, depending on the bank or loan provider. Check out our list of fast approval loans, which can process your application and disburse funds within 48 hours. These loans are an excellent option for urgent financial needs, potentially providing funds in as little as two days.

To improve your chances, focus on key factors lenders evaluate that can affect your personal loan approval:

- Credit score: Higher scores indicate responsible financial behavior.

- Income stability: Demonstrate steady earnings and employment history.

- Debt-to-income ratio: Lower ratios are favorable.

- Assets and collateral: Valuable assets can strengthen your application.

- Financial history: Past bankruptcies or defaults are considered.

While meeting these criteria doesn’t guarantee approval, understanding and improving these aspects can enhance your chances of securing a personal loan.

Follow these steps to boost personal loan approval odds:

- Check and improve your credit report

- Maintain a high credit score by paying bills on time and reducing debt

- Show stable income and employment history

- Consider offering collateral or a co-signer

- Research lenders and their requirements

- Prepare a list of assets and a clear loan purpose

- Be honest and thorough in your application, providing all required documents promptly

Following these steps will maximize your chances of loan approval.

Don’t let a personal loan disapproval discourage you. There are several steps you can take to improve your chances of approval in the future.

Steps that you can do if your personal loan application is rejected:

- Ask the lender for a detailed explanation on why your application has been rejected.

- Review your credit report for errors and dispute any inaccuracies.

- Improve your credit score by paying bills on time and reducing credit card balances.

- Explore alternative lenders or loan options.

- Consider adding a co-signer with good credit.

Stay persistent and focused on your financial goals. By addressing these issues, you can increase your chances of approval in future applications.