Need Fast Cash? Here’s How Find The Best Personal Loan

Table of Contents

If fast money is what you need, then the best banking product that can get you out of a tight spot is an unsecured personal loan. Though it is relatively easy and fast to get one, it is also one of the most expensive and riskiest loans available.

With high interest rates and short tenure (maximum of 10 years), it can be quite difficult to pay back on time. However, if this is really your only option and if you have a stable income every month to commit to the monthly repayment, then you need to know a few tricks to find the best deal.

When shopping for a personal loan, you should consider these points – the interest rates, the maximum tenure, the minimum loan amount and other additional cost involved, if any.

But which is the best one out all these features? Here is a step-by-step guide that will lead you to the best loan for your financial needs:

1. Interest rates

As with any loan, the lower the interest rate the better. Although most personal loans offer a fixed rate, there are some that offer effective interest rates. Essentially, for a borrower who intends to pay the loan on schedule for the whole tenure, there isn’t much of a difference in the payments.

However, if you are planning to clear off your loan before the tenure is up, a fixed rate loan may just save you some cash.

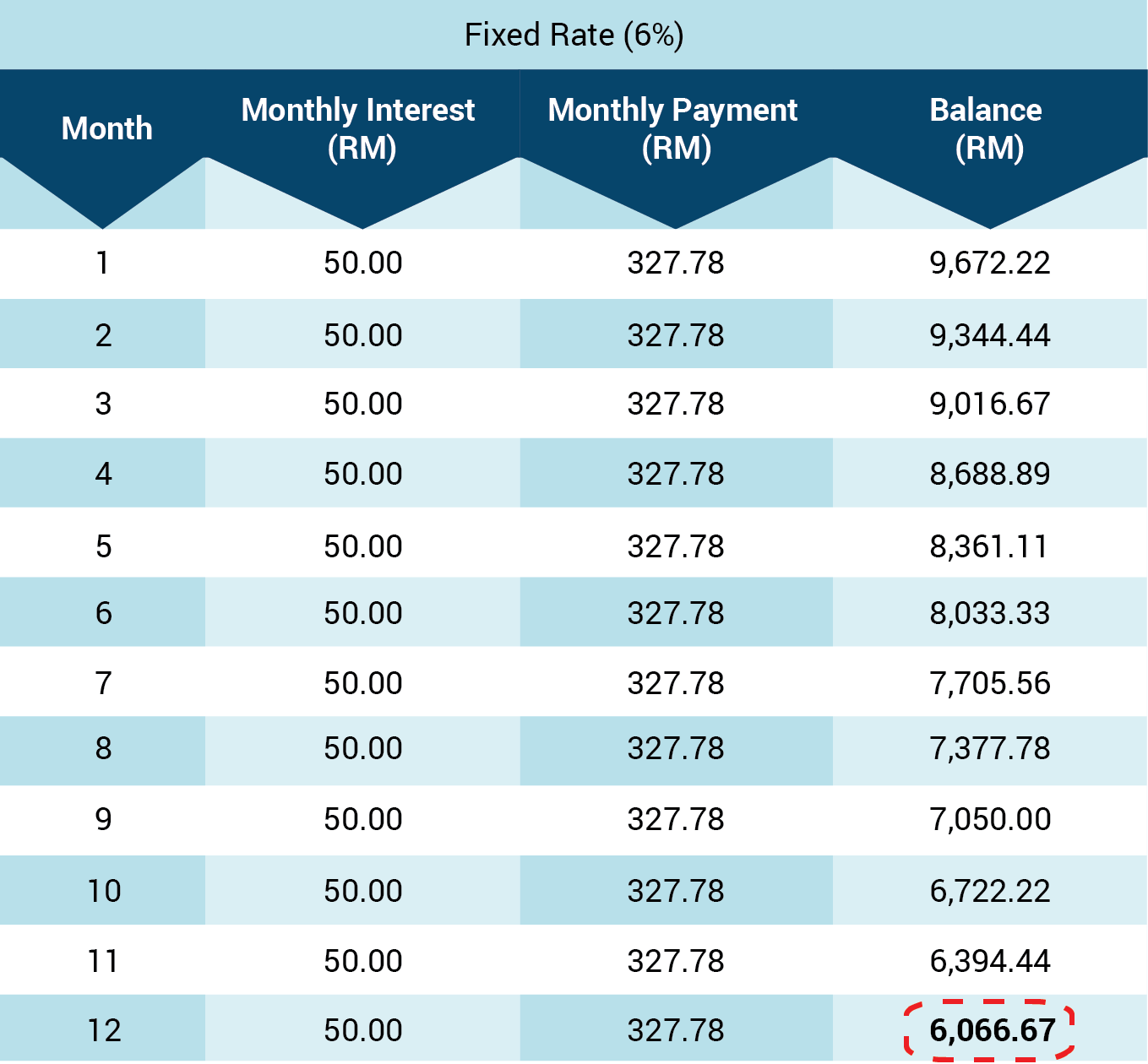

Fixed rate loan

For example, if you are borrowing RM10,000 for a 3-year loan and you would like to pay off your loan on the first year, here’s how much you have to pay for fixed rate and effective interest rate loans:

Loan amount: RM10,000

Annual interest rate: 6%

Loan tenure: 3 years

At the end of the first year, you will need to pay RM6,066.67 to clear your loan.

Effective rate loan

At the end of the first year, you will need to pay RM6,864.06 to clear your loan, that is RM797.39 more than fixed rate.

Loan cost

However, we cannot just take up a loan solely based on the interest rates. Sometimes the lowest rates offered may not be the best offer.

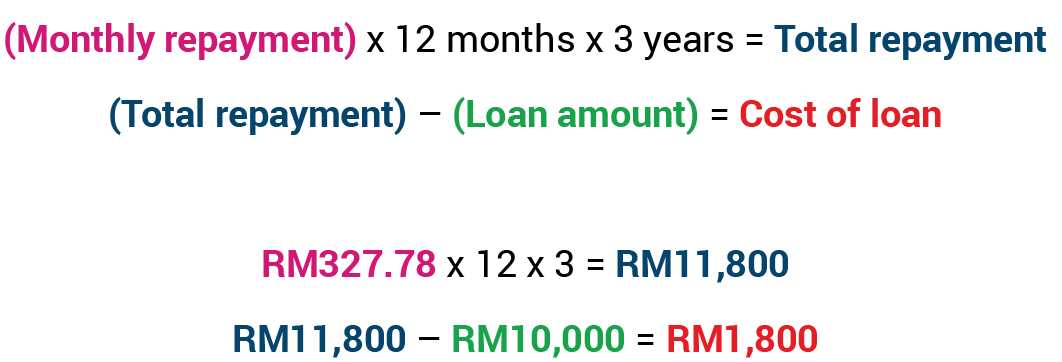

To find out if the loan is worth taking out, calculate the cost of your loan. Just check the monthly repayment using our online calculator. In the example above, with 6% rates per annum, you will be paying RM1,800 over three years.

2. Loan tenure

As of March 2013, Bank Negara Malaysia (BNM) restricted the maximum loan term for personal financing to 10 years.

Though it is the maximum tenure allowed, most banks do not allow a 10-year term on their loans. Some banks do state that the maximum tenure is 10 years. These include BSN, Bank Islam, Maybank (salary financing product), Co-opBank Pertama and Bank Rakyat (Financing-i Public Sector). However, it is not a guarantee that you will qualify for the maximum loan tenure.

3. Loan amount

Depending on your financial need, you may need to look for a bank that lends enough to cover your situation, so check the maximum loan amount first.

The interest rates vary wildly, depending on the loan amount but avoid anything above 10% if at all possible. The maximum loan amount offered currently is RM150,000 and the minimum is RM1,000.

Whichever amount you decide to apply for, always make sure that you will be able to commit to the monthly repayment.

4. Other costs

Certain personal financing packages require processing fees, stamp duty (maximum 0.55% of loan amount) and disbursement and other miscellaneous fees. These are all one-time cost to be paid before disbursement.

Other considerations include the option for early settlement of the loan. Some banks require borrower to pay RM200 or sum equivalent to 3% of outstanding loan amount, whichever is higher for early settlement of within the first half of the loan tenure. If your loan tenure is three years and you settle your loan within the first 1.5 years, this penalty will be imposed.

Most banks also charge late payment charges of about 1% of the outstanding loan amount. If your outstanding balance is RM6,000, it will be RM60, which can be quite costly if you often miss your payment due date.

5. Approval duration

For those who are really looking for quick cash, this can be a deal breaker. Don’t worry though, due to stiff competition among banks, the approval duration for this type of loan can be as short as one hour. Check out your options on fast approval loans here.

6. Requirements

Banks will require you to be at least 18 years old but below 60 years old, and have a current source of income. Some loans may be restricted for full-time employees of private organisations, while others may be open to government servants and self-employed individuals.

Borrowers may also be required to have a linked savings account at the bank or purchase a Takaful product with the bank before they can apply for a personal financing with the bank.

However, not every loan service requires all that. To choose the ideal loan, the borrower will need to weigh all pros and cons and find one that suits their needs.

Although many companies can lend up to RM100,000 or more, you should be careful and conservative when choosing an amount to borrow. Keep in mind that the best personal financing is intended to help you out in a crisis but because of its high interest rates and short payback terms, it is never an ideal long-term financial solution.

Using our personal loan calculator, compare and consider all the loans and options. It can help you make a smart decision when it comes to choosing a personal loan. If you borrow responsibly and pay the loan back in a timely manner, you won’t go wrong.

These loans are not financially beneficial or cheap; they’re simply good for quick emergency cash.