What Do You Do When Your Credit Card Debt Turns On You? Use Balance Transfers!

Table of Contents

According to Credit Counselling and Debt Management Agency (AKPK), 33.3% of Malaysians’ household debt comes from their credit cards.

“One of the reasons is lifestyle… they fall into the trap because of poor financial planning,” said Mohamed Khalil Jamaldin, head of corporate communications of AKPK to The Malaysian Insider.

However, racking up a high credit card debt doesn’t always have to make you fall into an endless debt spiral. Banks are offering facilities like balance transfer, which allows a credit card holder to shift debt from an existing credit card with a high annual interest rate to one with lower interest rate or even 0% rate over a fixed period.

Transferring this debt could save hundreds of Ringgit in interest repayments. However, choosing the wrong transfer card could land you into even more trouble.

Here are three recommended credit cards to transfer your balance to and how much you can save if you choose the right type for your situation.

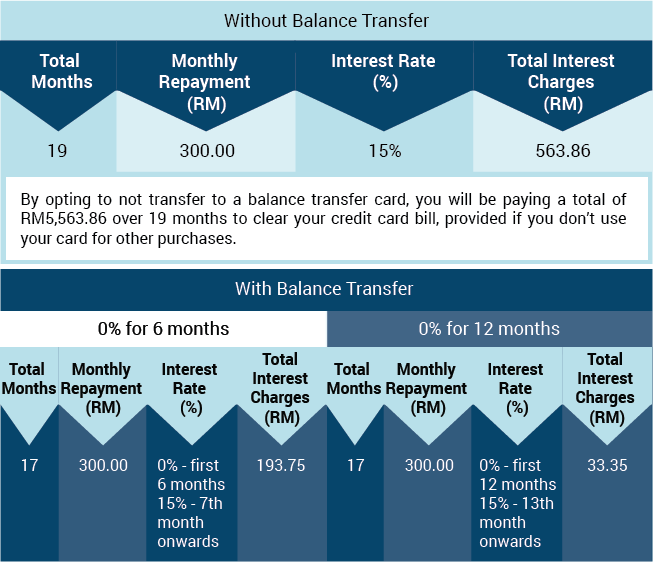

Scenario A:

If you have a RM5,000 outstanding balance on your credit card, and you are only able to pay RM300 a month, here are your options:

Based on the table above, by transferring your credit card debt to a 0% for 6 months facility you will end up paying more in interest compared to 0% for 12 months, saving about RM530.51 in financial charges compared to not transferring your debt at all!

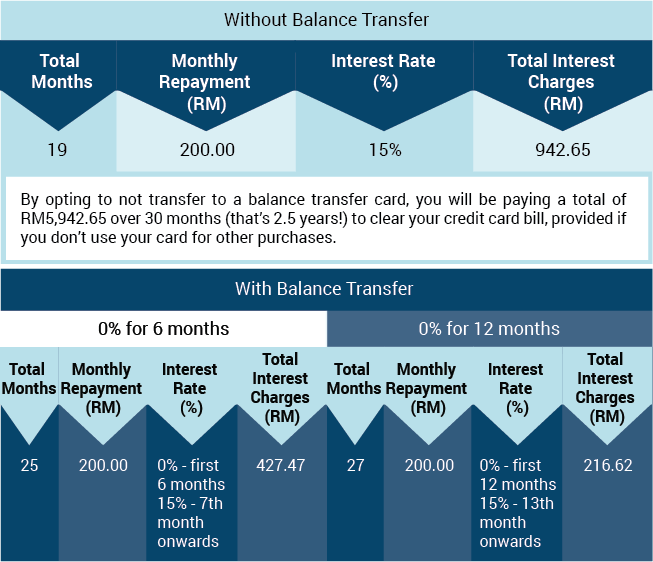

Scenario B:

With the same outstanding balance of RM5,000, but only be able to commit to paying RM200 a month, your most obvious choice is:

The obvious choice is the 0% for 12 month option as you will be saving RM726.03 compared to not have transferred to a balance transfer card at all. However, the downside of opting for the 12 months is most banks require a one-time upfront fee.

Other fees

Generally, these facilities require a 3% to 4% upfront fee. For a RM5,000 transfer, it will translate to RM150 for 3% and RM200 for 4%.

Scenario A: If you choose a 0% for six months with no upfront fee, like what Public Bank credit cards are offering, you will still be paying RM193.75 in interest. However, if you opt for a 0% for 12 months option with 2% upfront fee, you will incur about RM133.35 – still lesser than the 6 months option.

Scenario B: By choosing any of the Public Bank credit cards, the 12-month option will come with an upfront fee of 2%, which amounts to RM100 (that’s still over RM600 savings) and for Maybank credit cards, the upfront fee is at 3%, totalling to RM150 (saving about RM576).

Always read and understand the fine prints to get the best deal. Currently, Public Bank credit cards offer 0% for six months and 0% upfront fee too!

Other restrictions

Balance transfers are usually utilised by credit card holders who are finding it hard to pay their credit card in full monthly and promptly. Instead of defaulting on your card payment or just paying the minimum payment, these card holders should seriously consider utilising these credit cards. It’ll help you!

However, do note that there is a minimum transfer amount for the facility. Depending on the bank and the conditions, the minimum transfer amount can range from RM1,000 to RM5,000.

To take full advantage of a balance transfer, one must be confident that the total amount can be paid off in the period set out, or as set out in the example above, even if you are unable to pay off everything in the 0% period, you will still be saving on interest charges in the long run. Any outstanding balance will be charged the usual credit card rate, which is usually 15%.

Find out how much you can save with balance transfer.

* Calculation above is simplified to compound monthly for easier understanding. The interest is usually compounded daily from the transaction date.