Will KLIBOR-Based Home Loan Be A Game Changer?

Year 2014 has shaped up to be a financially challenging year for all – both consumers and investors.

Year 2014 has shaped up to be a financially challenging year for all – both consumers and investors.

With the rising cost of living and various cooling measures on the property market – consumers are still finding it hard to own their first home, and investors are forced to change their game plan on property investment.

On the other hand, borrowers looking to lock in a long-term fixed home loan are being urged to act quickly to secure the current Base Lending Rate (BLR) at 6.6%, which is at its lowest in the last 10 years.

What comes down, is likely to go up again. According to reports from The Edge, Bank Negara Malaysia (BNM) is set to outline a new framework for the country’s reference rate this year. Most are wary that the lending rate may be increased, adding salt to Malaysia’s economic wounds.

Update: On July 10, 2014, BNM announced an increase in the Overnight Policy Rate (OPR) by 0.25%, resulting an increase in the BLR to 6.85% by most major banks.

However, some investors on propertyWTF.com and bankers on i3investors.com are speculating that the new framework will be based on the Kuala Lumpur Interbank Offered Rate (KLIBOR).

It is the estimated average interest rate charged when one bank borrows from another bank in Malaysia.

The rate is determined by a daily poll carried out on behalf of the Finance Markets Association of Malaysia that asks 12 banks to estimate how much it would cost to borrow from each other. The highest and lowest submissions are excluded, and an average of the remaining 10 entries calculated to set the rate at 11 a.m. local time.

What is it?

Though KLIBOR-based home loans (Standard Chartered Mortgage KLIBOR and recently, Hong Leong KLIBOR Housing Loan) have been introduced in Malaysia’s property market since mid-2008, banks have not been aggressive in promoting these products.

This has made the interbank offered rate an uncommon term for most home buyers as mortgages based on this rate are not easily available in the market. The reason for its unpopularity could be due to its fluctuating nature and fast reaction to the economic sentiment.

As floating (variable) interest rate loans in Malaysia make use of BLR or Islamic Financing Rate (IFR) as its reference rate, similarly, the interbank offered rate is used as the reference rate to determine the price (interest rate) of a KLIBOR-pegged housing loan.

KLIBOR versus BLR

The main difference between the two rates is the fluctuating nature of the interbank offered rate, as the interest rate is reviewed and updated every three months to reflect the 3-month rate.

However, due to this regular revision, it is seen to be more transparent than the current reference rate, as the rate is published in major newspapers every day.

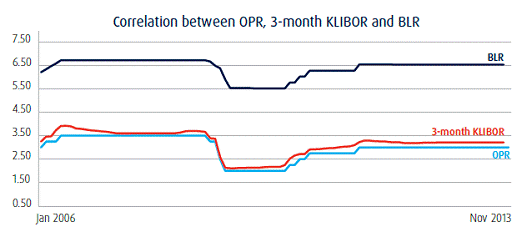

Historically, it has consistently been lower than the lending rate. However, it is not guaranteed, and there is a possibility that KLIBOR can overtake BLR, though very rarely.

The offered rate moves in the same direction as the reference lending rate but they don’t have the same momentum. For example, if BLR increases by 1%, KLIBOR will also increase but at a different quantum. Both rates are based on Overnight Policy Rate (OPR) set and regulated by BNM.

“The possibility of KLIBOR being open to rigging was lower compared to, for example, the London interbank offered rate (Libor), as the former was closely tied to the OPR which was determined and set by Bank Negara after considering liquidity and other related conditions,” said Chan Hooi Lam, Ernst & Young Malaysia partner, assurance (financial services) to The Star.

The bottom line

The interbank offered rate isn’t for everyone. With its fluctuating nature, it gives a sense of uncertainty.

If you’re applying for a home loan with its features, there are certain factors that must be considered before making the decision.

If you are averse to risk, fixed rate home loans are sometimes the better way to go, especially with the low lending rate offered right now.