3 Reasons Why Property Valuations May Not Be Accurate

Table of Contents

Other than your earnings and credit report (CCRIS), property valuation affects a person’s home loan eligibility, too. If the property is valued around the amount negotiated between the buyer and seller, the buyer will most likely be covered by a loan-to-value ratio of up to 90%.

Other than your earnings and credit report (CCRIS), property valuation affects a person’s home loan eligibility, too. If the property is valued around the amount negotiated between the buyer and seller, the buyer will most likely be covered by a loan-to-value ratio of up to 90%.

However, what happens when the valuated price of the property falls below the agreed price? Buyer and seller may have to renegotiate in view of the valued price, or call off the transaction. Sometimes the property valuer returns a lower value, long after you’ve agreed to buy the house. In this case, you will end up having to pay a much larger deposit than just the usual 10%!

So, why do property valuations and market value differ?

1. Prices rise quickly and steeply in a rising market

Property valuers rely on recent transacted prices from the Valuation and Property Services (JPPH), where the data on recent transactions are compiled over the most recent three and six months.

Hence, by the time the valuation report is issued, the valuation price may be outdated, especially in a bullish property market.

According to a report on The Star Property, Siva Shanker, president of Malaysia Institute of Estate Agents (MIEA) said, difference in valuation is a common occurrence when prices rise quickly and steeply.

When asked how buyers can obtain a higher mortgage to pay for lower down payment, Shanker said that most buyers have a lot of savings and would pay the higher upfront cost anyway.

Former JPPH director general, Dato’ Mani Usilappan backed the response saying that he had a client that was willing to pay RM75,000 for a house that was in a good location when there had been 10 other transactions going at RM60,000.

The maximum loan amount he could have gotten was RM54,000 (90% of market value), meaning he would have needed a minimum deposit of RM21,000 (or 28% of market value).

2. Project developers do not rely on values provided by valuers

Property developers are required by banks, whom they are getting project loans from, to appoint property valuers to come up with independent market research reports to ensure pricing of their properties are within market norms.

However, the developers don’t always rely on the findings on the reports.

According to property developer Vignesh Naidu of F3 Capital Sdn. Bhd., the values provided by valuers are not necessarily relied upon. He also said that loans are often obtained several months before the launch of a property, hence prices may be revised upwards.

This does not translate well for the buyers as the purchasing price is higher than the valuation figure a buyer should get.

3. Stiff competition among banks

Valuers often have to bend to the will of bankers due to the stiff competition in the home loan market.

It is not uncommon for a homebuyer to approach a few banks to shop for the highest possible valuation and thus higher housing loan, which creates competition amongst banks. To ensure they secure the borrower’s business, the bankers will in turn shop for the highest values, which creates competition among valuers to give each banker the highest possible valuation in order to keep the banker’s business.

According to the same The Star Property report, veteran chartered surveyor and valuer, Dr. Ernest Cheong reveals that some Malaysian bankers have requested valuers to value properties above their market values for loan purposes while some have requested for an undervaluation of foreclosed properties to be sold by public auction to benefit certain parties.

Why is property valuation important?

Having an accurate estimation of a property’s value is important to both parties in a home-selling transaction, but more so for the buyer to enable him or her to make a reasonable and justifiable counteroffer and to determine if the upfront cost is affordable.

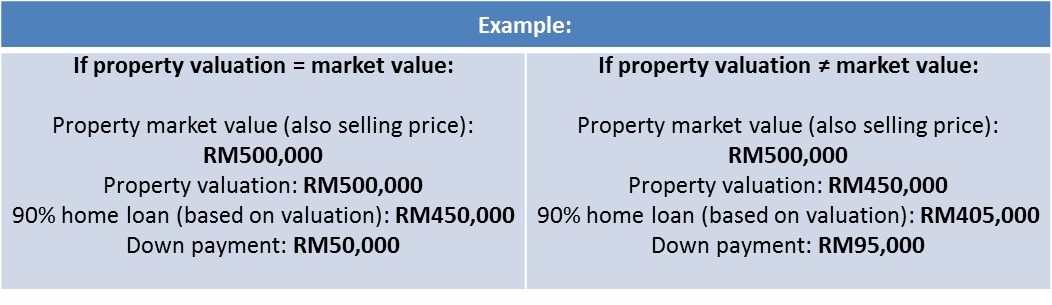

Often, the 90% (or lower) margin of finance provided by a bank is based on the valuation of the property; not the purchase price. A lower property valuation means lower loan amount, and since it is unlikely that a seller would be willing to sell below the market value, the buyer will have to come up with more money to cover the upfront cost.

From the examples above, a lower valuation will result in a RM45,000 increase in upfront cost which the buyer may not have, thus making the home unaffordable. To make things even worse, if the buyer has already paid the booking fee before obtaining the valuation, the amount paid will be forfeited if the buyer decides not to buy the property.

Therefore, it is important for the buyer to ensure the booking receipt issued by the seller or the agent includes a clause that states that buyer is entitled to a refund of the booking deposit in the event of unsuccessful loan application.

To avoid this from happening, buyers should always apply for a home loan from more than one bank to get the best valuation price and loan offer.