Wealth Management Isn’t Just For The Rich

Table of Contents

Whether you are a young couple who want to save for the education of your newly arrived bundle of joy, a middle aged couple planning for retirement, or the main breadwinner for your family, you still need wealth management.

Wealth management is basically a combination of investment management and financial planning.

Investment management is about the art and science of making proportional investments into equities or bonds which includes asset mix selection, security selection and monitoring. On the other end, financial planning often involves structuring personal financial affairs such as managing income and expenses, tax planning, will and estate planning, credit and lending, and insurance. Both have a common goal of achieving our personal or financial objectives.

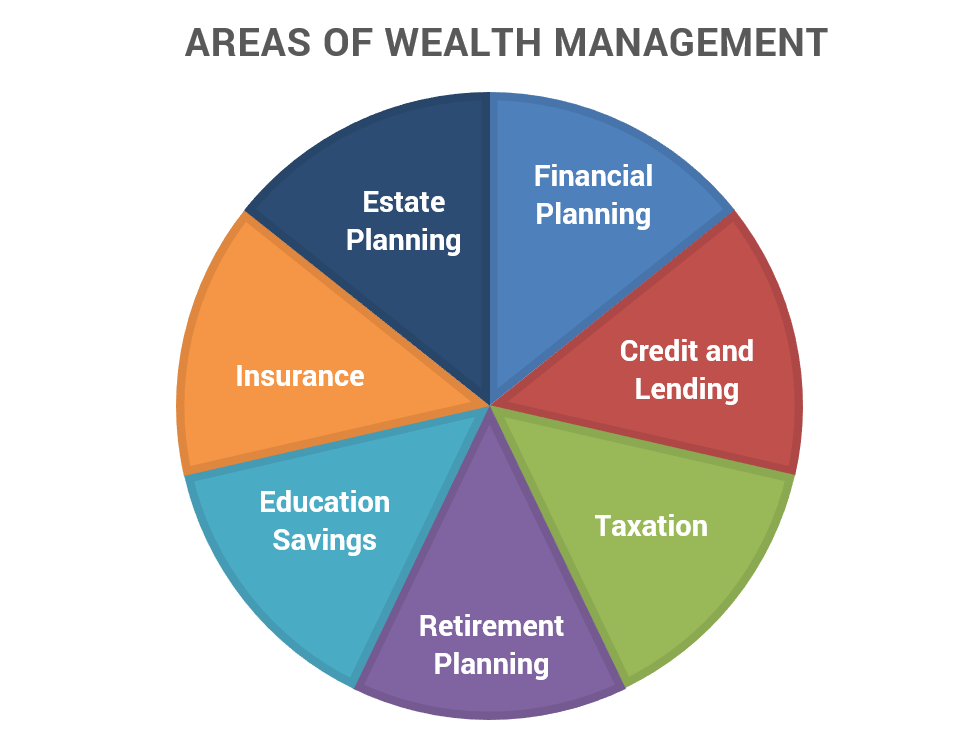

Wealth management can loosely be divided into seven categories of financial commitments that all of us are, in some way, committed to.

With the aim to accumulate and preserve, wealth managers put into place a strategic financial roadmap according to an individual’s needs. Therefore, it is only natural to include all the elements of your financial status and needs in order to create an efficient money management system.

When done effectively, one can potentially reduce investment risks, taxes and unnecessary expenses while improving financial returns and increasing assets. It works for providing both efficient consumption of assets during one’s lifetime and efficient transfer of assets in death.

Why is wealth management not just for the rich?

Managing your money helps to determine how best to invest and save in order to meet your various financial objectives – which could help you in accumulating, managing or preserving the wealth. An ordinary individual would require wealth accumulation more than their rich counterpart as they would have more pressing money needs compared to the latter which would be focusing more on wealth preservation.

A. Having a sustainable retirement

Everybody needs to plan for their retirement, regardless if they are public sector employees who are funded by their pension scheme, private sector employees who have their Employees Provident Fund (EPF) savings, or self-employed, who basically has to acquire their own personal savings.

According to a recent survey by the Department of Statistics Malaysia (DOSM), almost three quarters of Malaysian employees said that their savings can only last for two months while those who have worked for over 30 years had sufficient savings for only four months. Considering that the average lifespan of a Malaysian individual is 75 years, we must be able to generate enough income to support ourselves for at least 15 years after retirement based on the official retirement age currently set at 60 years old.

Meanwhile, EPF statistics show that 65% of retirees can only afford to spend RM208 per month. This amount is not practical as they would need to cater for their general expenses, healthcare, ongoing debt repayments, etc.

To truly enjoy retirement, you must have enough savings to cover your expenses or produce streams of passive income such as dividends from investments or work out a retirement plan.

A wealth manager will be able to advise the best way for you to save up for your retirement – from the right investment vehicle to the total amount you will need by the time you reach retirement. If you are not already contributing to EPF, you can start saving for your retirement using the private retirement scheme (PRS) or on EPF’s i-Saraan if you are self-employed.

B. Saving for a child’s education

There can never be a greater gift than leaving your kids with the best education you can afford. Cost of obtaining an education can be intimidating especially at private colleges (above RM60,000) and overseas universities (above RM200,000), with education costs escalating at a fast rate. Without an education savings, they will have to opt to study loans such as PTPTN or work their way to a scholarship.

To save and generate enough funds to pay for tertiary education in 18 years’ time, parents need to look into different investments that will fit their needs and risk tolerance. A wealth manager will be able to advise on the best course of action. Some of the options are government bonds, unit trusts, capital financing, and real estate.

For those who have bigger risk appetite, they can invest in commodities, gold or FOREX. These investment have higher risks but may provide the investors with substantial investment returns in the long run.

C. Making sure your family is financially secure

Insurance is an integral part of any financial planning. It is necessary to have adequate insurance coverage to ensure that you and your family are protected financially against unforeseen circumstances. Based on your needs, you can invest in a life insurance, medical insurance, home protection and many other options to choose from.

The key is not just to get insurance coverage but to get adequate coverage. With proper wealth management, an individual will know the sum insured that is considered adequate, based on the family commitments and affordability.

D. Ensuring your wealth gets passed on smoothly

Wealth management, done correctly, can potentially grow your money and assets over time. Therefore, it is important for you to ensure you assets are properly assigned to the right beneficiaries if anything unfortunate were to happen to you.

Identify your investment beneficiaries to ensure your hard earned investments are passed on to your loved ones with minimum legal formalities. It will be a moment of grief and it would not be fair to put them through another hassle of sorting out the financials.

E. Managing your short term goals

You could very well have shorter term financial goals such as buying a car, saving up the down payment for a new house, furnishing your new home, or even, travelling. For these goals, you may want to consider investing in share financing, money market or fixed deposits as they provide you with high liquidity and has lower risk considering the short time line.

A balanced wealth management portfolio should consider the long term and short term goals before coming up with an effective strategy to meet all the goals based on the current abilities.

Everyone needs wealth management

In other words, money management plays an important role in realising our personal and financial dreams by taking a multi-disciplinary approach which enables us to plan for a broader set of opportunities and risks. Wealth management may be the key to peace of mind and financial security for all.

The nature of this management doesn’t mandate that only the wealthy can benefit. In fact, everyone, regardless if you are making RM30 million, RM30,000 or RM3,000 monthly, needs a robust financial plan.

No matter how much you earn or own in wealth right now, you still need to make a plan to protect, grow and ensure the wealth you accumulate can continue to increase over time.

This article has been updated on June 21, 2024.