8 Steps To Manage Your Money During COVID-19

We’re all aware of what’s going on in the market today. Some call it the perfect storm – crippling effects of a viral pandemic, an unexpected change of government, a dramatic drop in oil prices … and the list goes on. When we look at the value of our investments compared to the start of the year, we can’t help but wonder if it’s better to sell out first to weather the storm, before reinvesting when the water is calmer. Fortunately, COVID-19 and its effects are deemed as events. And we have historical data to give us some idea on what to expect when faced with such events.

If we can leave you with just one thought to ponder on this matter (given that you’ve probably been inundated with various views already), it’ll be this: Time in the market is superior to timing the market.

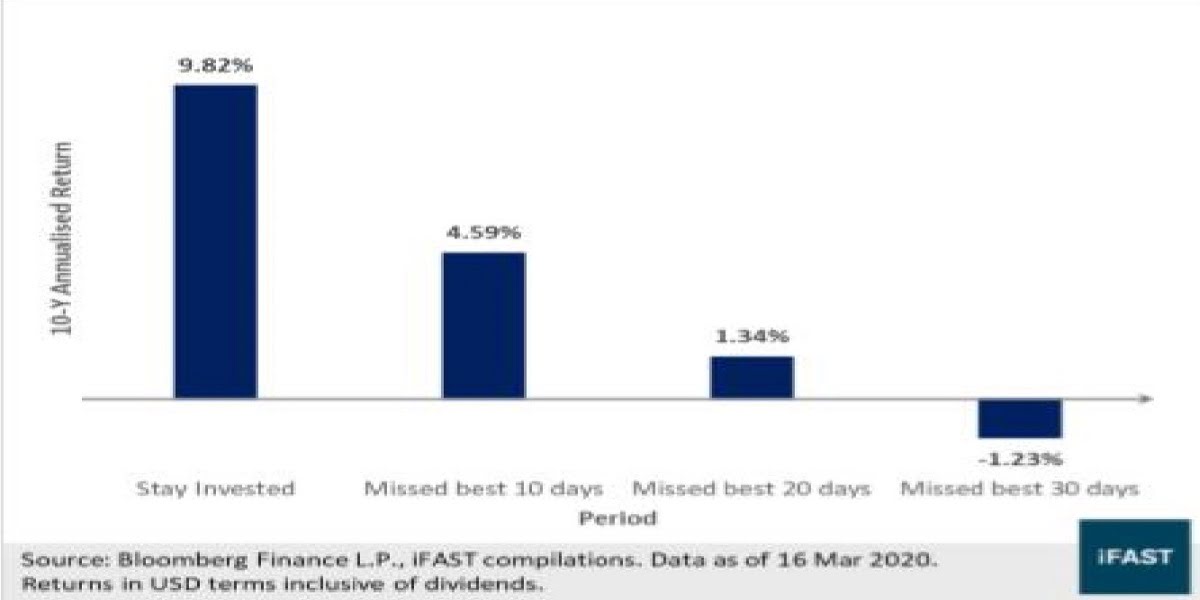

Source: Bloomberg Finance L.P., iFAST compilations

If you started to invest after the Global Financial Crisis (March 2010), you would have gained a 9.8% annualised return as of 16 March 2020 – a very impressive feat considering that the figure is inclusive of the drawdown over the last two weeks. However, if you missed the best 10, 20 or 30 days of the market during this 10-year period, your investment returns would have paled in comparison. As such, we continue to take comfort that unless we have a crystal ball, our better bet is to remain invested. Nevertheless, what can we do in such trying times?

We would like to propose (or remind you about) the 8 steps to manage your money more effectively any time (the golden rules):

1. Ensure that you have the required cash reserves in place

- If job / income security is not a major concern – then ensure you have at least 6 months’ worth of expenses as cash reserves. Otherwise, increase this as you deem fit. Retirees should have at least 3 years of expenses as cash reserves

2. Review your risk profile and remain invested according to your risk tolerance

- If your risk profile is unchanged – remain steadfast with your current investments. Otherwise, consider reducing the risk level of your investments by a notch or two if it helps you sleep peacefully at night

3. Invest according to your strategic asset allocation

- Review your ideal allocation of investable assets in low, moderate and high-risk assets. If you have too much in any asset class – consider rebalancing your position

- Investing according to your ideal strategic asset allocation will ensure a more robust and resilient long-term growth (a.k.a. growing your money with higher certainty)

4. Remain diversified

- Ensure that you invest in diversified portfolios that span across different asset classes (local bonds, regional/foreign bonds, local equities, regional equities, global equities, REITs, commodities, etc.), geography (Malaysia, regional, global) and currencies

5. Remember your purpose for investing

- Are you investing for your retirement, child’s tertiary education, purchase of a new property, a wedding or a pilgrimage? Has the timeline for these goals changed? If these haven’t changed, perhaps you shouldn’t too

6. Be greedy when others are fearful

- If you have cash on hand after fulfilling all the steps above, then consider this a special offer period with steeply discounted prices. As such you should look for buying opportunities

- We can’t be sure when’s the bottom, so stagger your investments to pick up on dips. Once you strategise your investment approach – follow through over the pre-set time frame

7. Review and monitor

- As things remain fluid, do continue to review and monitor your financial position and take the necessary corrective action, if any

- This does not mean that you should track the performance on a daily basis as this might emotionally trigger you to take actions that you might later regret

- Remind yourself of your “WHY” to invest … and stay the course

8. Get a second opinion

- If all the above seems daunting to do alone, seek advice from our licensed financial planners for a second opinion

- Now is as good as any time to start charting your holistic financial plan (if you haven’t got one yet) for better clarity, confidence and control over your finances