Malaysia Sees Sharp Increase In Health Insurance Premium

Table of Contents

Malaysians have recently been hit with various price hikes since middle of last year. The announcement of another hike comes as no surprise, though not without exasperation from the public.

On April 20, 2014, The Star broke the news of insurance companies increasing their charges and premiums of medical, health and investment-linked policies by up to 20%. This is due to the rising medical costs.

As quoted by The Star, Kho Chui Ing, the deputy president of National Association of Malaysian Life Insurance Field Force and Advisers (Namlifa), said most companies had adjusted their charges and premiums for medical, health and investment-linked policies over the last few months to cope with medical inflation.

Why the increase?

In December 2013, the Government allowed a maximum 14.4% rise in private medical fees – almost half of the 30% requested by the Malaysian Medical Association (MMA). Though the medical cost has not been permitted to increase for the past 12 years, this recent increase comes like a ripple effect after various price hikes.

Due to this medical inflation, insurance coverage prior to the increment may not be able to cover the medical cost incurred by policyholders.

According to a Bank Negara Malaysia’s (BNM) official, insurance premium is set by insurance companies using actuarial principles. Factors affecting the premiums are exposure to anti-selection risk and medical inflation.

“There are, however, safeguards in place. Insurance product pricing requires a qualified actuary of the insurance company to certify the reasonableness of the premium charged.

“This is influenced by economic factors such as medical inflation, mortality and morbidity rate as well as investment performance of the insurer,” she said to The Star.

How would a 20% increase impact your bottom line?

The worst impacted policyholders are the high risk individuals, especially those who are aged and had past medical conditions.

For a relatively healthy individual in her thirties, a medical coverage of RM733 may cover hospitalisation and fees of up to RM100,000 a year. With the 20% increment, she will have to pay RM879.60. A RM146.60 increment a year.

The pinch would be felt by those aged 38 and above, with senior citizens quite possibly paying more than RM100 extra a month. The higher your health insurance premium is, the higher your increment will be. Furthermore, the older you get, the higher the premiums will increase.

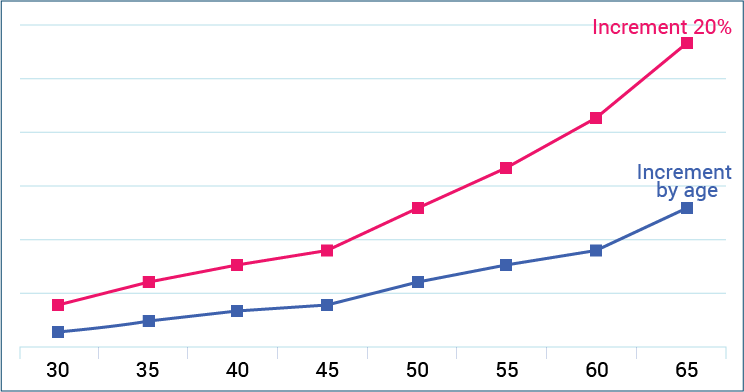

Here is a graph to illustrate the increment:

Note: This graph merely illustrates the increment in premium over time, assuming that the increment of 20% remain until the individual reaches 65 years of age.

Employers who provide medical insurance to their employees will also see a significant impact in the cost due to the increment.

According to Datuk Shamsuddin Bardan, executive director of the Malaysian Employers Federation (MEF), said an employer pay an average of RM850 per employee per year for medical insurance premium.

He added that about 8% of 6.5 million employees in the private sector were covered by insurance, which comes up to 520,000 employees. Based on this figure, private companies are estimate to spend RM442 million on medical insurance premiums per year.

With the increment up to 20%, this expenditure may go up to RM530.4 million – a whopping RM88.4 million increment!

Do you have a choice?

Traditionally, the increment is applied on upgraded products only, but for this recent increment, insurance companies are increasing charges and premiums on existing policies. Hence, policyholders must comply with the new rates or risk their policy lapsing.

With the rising medical cost, the public, especially the elderly, may not have other alternatives to cover their medical fees. Though the costs of medical and health insurance are increasing, it is still the best option to protect oneself from insurmountable medical cost in time of needs.