Investing With Ringgit Cost Averaging: The Good, The Bad And The Ugly

Table of Contents

This article is sponsored by Securities Commission Malaysia, under its InvestSmart initiative.

If you think you need a pool of cash to gets started in the world of investment, you may want to read this. Ringgit cost averaging (RCA), a commonly adopted investment technique, may just help you realise your investment dreams without first having a million bucks.

What is RCA?

Ringgit cost averaging means investing a fixed amount at fixed intervals. For example, putting RM200 every month into your unit trust fund investment, as opposed to putting a huge sum of money into the investment fund at one go.

Essentially, what this translates to means you end up buying more units when the unit price is low, and when the price is high, you would be buying fewer units.

There are two strategies to RCA. Some investors may invest 20% of their monthly income religiously until they retire, while others believe in RCA a set sum of money. For example, instead of investing RM2,400 in a lump sum, you may break it down to RM200 monthly for 12 months.

Investors consider the first strategy a sensible approach to investing because they will be committing a fixed amount of their salary every month toward their financial goals, be it retiring in the Bahamas or buying their dream five-bedroom bungalow.

On the other hand, the rationale behind the second strategy is in hoping that market volatility would work in the investor’s favour, because they would automatically be purchasing more shares when the price is low, and fewer shares when the price is high. This method helps to spread out the risk factor over a period of time, and is especially useful if an investor is unsure of whether to do a bulk purchase at that point of time.

How does it work?

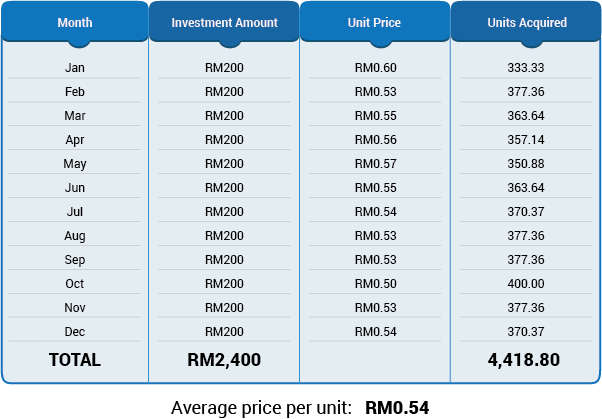

The table below depict how an investor averages out the unit price over a number of months by investing in a fixed, monthly amount amidst the Ringgit prices fluctuations.

Table 1: Ringgit cost averaging

Looking at Table 1, does the RCA method really yield higher returns compared to lump sum investing? The answer is yes, and no. The success of any investment really just depends on the market and timing. In the case of RCA, it primarily reduces your timing risk.

If you invested a lump sum of RM2,400 in January of the first year, the number of shares you could buy with that amount would have been 4,000 units. However, using the RCA method, you would instead have a total of 4,418 units by the end of the first year with the same amount invested.

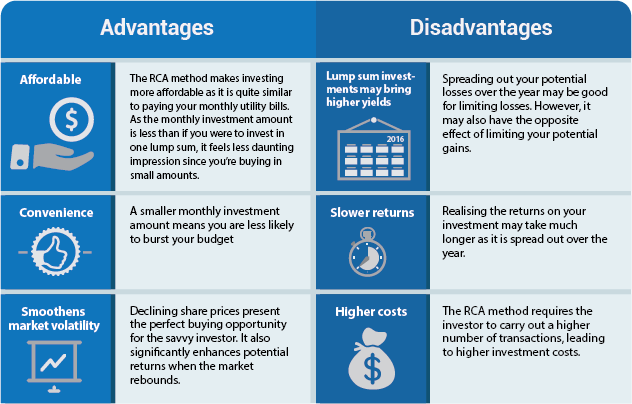

What are the pros and cons of the RCA method?

How do you win at this game?

Returns are not guaranteed with the RCA method, or with any other investment strategy for that matter. If the fund price of the investment units decline and do not manage to regain their standings, you could stand to make losses. However, in general, the RCA method does reduce the risk of investing all your assets at the peak of the market cycle.

Here are a few things you should consider in order to make gains with the RCA method:

- The higher the investment amount, the longer the investment time span. If you are planning to invest a large amount, RM100,000 for instance, you may want to spread it out over a period of 36 months — or three years — making it a monthly investment of RM2,777.77.

- Diversification is key. The RCA method alone is insufficient to minimise your risk. You will need to diversify your investments into various categories and rebalance this basket at least once a year.

- Understand your investment. Even with a relatively lower risk method such as the RCA, investors should still take the time to fully understand their investments.

- Letting go when objectives have been met. Every portfolio has its objectives. If you are investing with an objective to purchase property, you should sell off your investments once your returns are adequate for your objectives. Not selling means assuming more risks than is necessary. You can always commence another portfolio which adopts a similar methodology for a different objective.

Who should adopt this method?

The RCA method works best for these types of investors:

- Investors who have a store of cash for investing or a constant cash flow and are interested in high risk investments (to reduce their risk);

- Investors who are not adept at forecasting short-term market movements;

- Investors who are unsure of the right moment to make the move into investing; and

- Investors who have a long-term investment horizon.

If you fall into any of the categories above, you should consider the RCA method of investing. Do not, however, limit yourself to just one investment strategy. Different investment products, or even funds and shares, may require different methodologies.

The RCA is far from being the perfect investment methodology. Some people are quick to dismiss it, while others use it without fail in all their investments. Making the most of the RCA method is in knowing when to use it. The best investment strategy, if used for the wrong purpose will still lead to losses. It would also be wise to remember that you need not employ just one lone strategy, successful investors utilise a mix of investment approaches and consider their risk appetites and level of understanding before making their investment decision.

© Securities Commission Malaysia (SC). Considerable care has been taken to ensure that the information contained here is accurate at the date of publication. However no representation or warranty, express or implied, is made to its accuracy or completeness. The SC therefore accepts no liability for any loss arising, whether direct or indirect, caused by the use of any part of the information provided. The information provided is for educational purposes only and should not be regarded as an offer or a solicitation of an offer for investment or used as a substitute for legal or other professional advice. For enquiries regarding sharing, republishing or redistributing this content please write to: admin@investsmartsc.my.