Property Financing: Are The Banks Still Lending?

Recent news has been rife with news on property purchasers’ concerns on property financing due to the ever tightening of lending policies being put in place by Bank Negara Malaysia (BNM).

Like most developing countries, Malaysia has gone through tremendous changes in policies. These policies, though targeted at property speculators, are also affecting genuine home buyers.

However, Malaysia’s property policies are still not as stringent as Singapore, Hong Kong or even the United Arab Emirates (UAE).

The measures taken by BNM are inevitable as it’s in their interest to prevent Malaysia from falling into subprime crisis similar to what happened in the United States which sparked the last financial crisis. What BNM has done is timely to manage and regulate the market, as well as to avoid the economy in Malaysia from collapsing.

Since the introduction of the first lending policies back in 2010, the annual loan growth has slowed down to an average of around 10% – a healthy sign for the market.

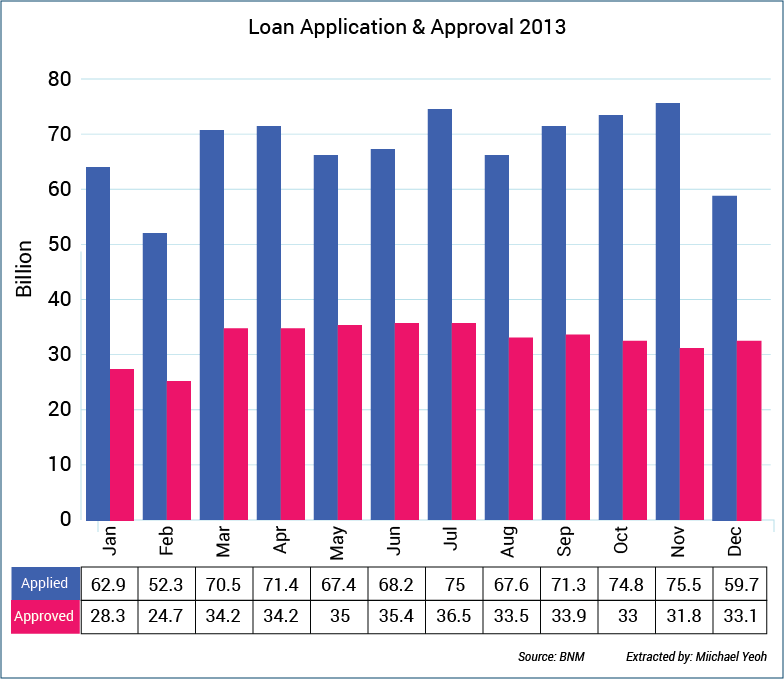

In 2013, total loans applied through banks came up to RM816.6 billion, but the loan amounts approved only netted RM396.3 billion. On average, for every 10 cases submitted to the banks, five will be rejected. This is rather alarming.

Developers with new projects launching, will have to look for at least 400 buyers for 200 units of condominiums. Why? The statistic above speaks for itself.

All is not lost

It is not impossible to borrow from the banks. The banks will still need to give out loans in order for them to profit. More than a decade ago, loan approvals were far easier, requiring only three months’ salary slips for approval.

Today, the rules have change tremendously. Borrowers will need a complete set of financial documents backed by proof of income earned before banks will even consider processing your loan.

In order for loan borrowers to get their home loans approved without too much trouble, there must be proper planning and understanding of the basic lending rules before submitting any financial documents to the banks.

There are three important things that a loan borrower needs to know before applying for a loan:

1. Make sure you are not in the Credit Tip-Off System (CTOS)

Managed by a private company, banks, legal firms, insurance companies and businesses use this system to check credit worthiness of their clients. If a person is being sued for bankruptcy, his or her name will appear in CTOS.

This applies to guarantors as well. Many CTOS listed individuals were denied loans as their names are listed in the system when they offered to stand as a guarantor for another person’s loan.

If the main borrower does not pay, the guarantor will have to pay and if the bank cannot locate or depend on the guarantor, both will be sued for bankruptcy. A bank will always reject this type of borrower.

Everyone can check their CTOS status online by providing the required personal particulars.

2. Central Credit Reference Information System (CCRIS)

CCRIS is managed by BNM. It provides credit data from various financial institutions in which are processed and automatically updated into the system. Financial institutions get access to the credit report by submitting a request to the system.

The system will show your complete credit history; how many loans you have and their amounts, credit cards, loan applications and also rejections. It will also have all your repayment records for the last 12 months.

If the person is a bad paymaster it will reflect in the system. Banks use this information to either approve or reject a loan application. It is recommended for a loan borrower to check their CCRIS report to ensure it’s clean before applying for a loan.

3. Debts Service Ratio (DSR)

Every person who is earning an income and has a debt will have a Debt Service Ratio (DSR). Banks uses this as a yardstick to determine credit approval for loan borrowers. Know yours first before going to the bank and apply for a loan.

Here’s how it is calculated.

Formula: Debt/Net Income X 100%

For example:

Debt = RM750

Income = RM1,000

DSR = RM750/RM1000 X 100%

= 77%

Since the implementation by BNM to take net income instead of gross in the calculation, many were worried about the impact this ruling will had towards loan approvals. The truth is, this new ruling has no impact on your loan approval because banks have also adjusted their approval criteria to match the ruling.

Before the implementation, banks’ DSR approval lingers around 50% to 70%. Different banks have different debt service approval criteria. Today there are banks giving up to 85%. Now, if you know your DSR is 75%, go to banks that have higher debt service approval and your chances will be much better.

Armed with the above information, you can save a lot of time in your loan application process by checking all the requirements for home loan approval before deciding on your dream home.

Looking for a home loan but unsure of your financial standing? Get expert advice from our mortgage consultant by applying for the best loan on our mortgage calculator.

Contact us at hello@imoney.my if you require more information on applying for a home loan.

Miichael Yeoh with over 18 years of experience in banking and finance, has handled more than 1,000 mortgage cases in his career. Currently, Yeoh is the Director and Founder of GM Training Academy PLT and Victorious PLT. With his vast experience, Yeoh is now a sought-after speaker in property exhibition and developer property launches in Malaysia and overseas. He is also the author of Think Like a Banker, Act Like A Player.